From enthusiasm to rationality: the maturity of cryptocurrency venture capital

Original article by Thejaswini MA

원래 번역: Block unicorn

머리말

I used to get excited about every 암호화폐currency funding announcement.

Every seed round seems like breaking news. “Anonymous team raises $5M for revolutionary DeFi protocol!”

I would research the founders like crazy, dig into their Discords, and try to understand what was so special about the project.

Fast forward to 2025. Another funding round pops up in my headlines. Series A. $36 million. Stablecoin payments infrastructure.

I categorized it under “Enterprise Blockchain Solutions” and moved on to other things.

When did I become so…pragmatic?

For the first time since 2020, late-stage cryptocurrency venture capital deals exceeded early-stage deals.

65% versus 35%.

Read it again.

This industry was once built on pre-seed funding, with anonymous teams building DeFi protocols in garages and innovating.

Now? Series A and beyond are driving the money flow.

What has changed?

Everything has changed. And yet nothing seems to have changed.

Crypto Venture Capital

VCs in suits. Due diligence went from minutes to months.

Regulatory Compliance. Institutional Adoption.

Professional project pitches, not anonymous Discord messages.

KYC process. Legal team. Really meaningful revenue model.

Companies like Conduit raised $36 million for “unified on-chain payments.” Beam raised $7 million for “stablecoin-based payment services.”

These are infrastructure projects. B2B solutions. Enterprise-grade platforms.

Boring, profitable, scalable business.

Crypto VC headlines love to exaggerate numbers, so let’s start with the facts:

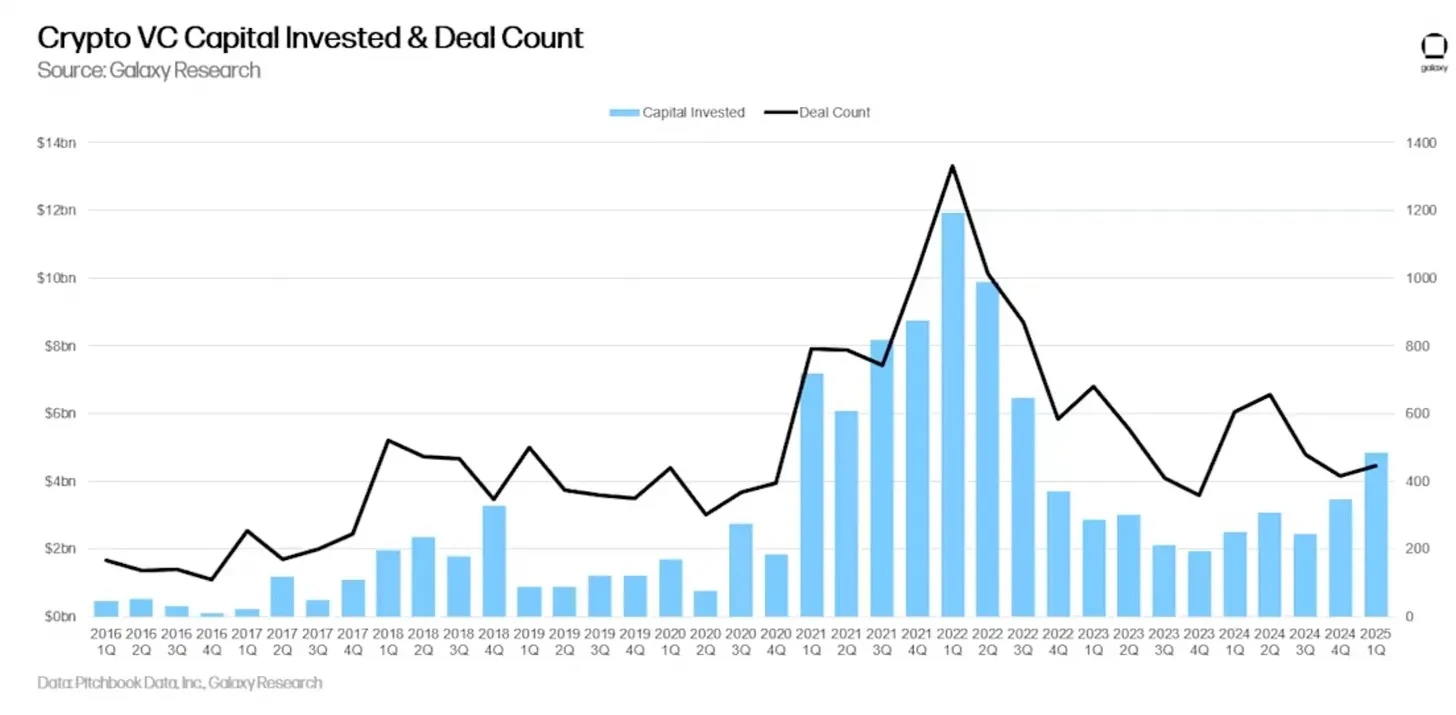

Q1 2025: $4.9 billion invested in 446 deals (up 40% QoQ).

Year to date: $7.7 billion raised, on track to reach $18 billion by 2025.

And here’s the thing: MGX (Abu Dhabi sovereign fund) wrote Binance a check for $2 billion.

This perfectly reflects the current venture capital environment: a handful of huge deals skew the data, while the overall ecosystem remains sluggish.

According to Galaxy Research, the correlation between Bitcoin prices and venture capital activity — which had been reliable for years — broke down in 2023 and has yet to recover.

Bitcoin hits new highs while venture capital activity remains sluggish. It turns out that institutions don’t need to fund venture startups to gain exposure to the cryptocurrency when they can buy a Bitcoin ETF.

A reality check for venture capitalists

Cryptocurrency venture capital falls 70% from a peak of $23 billion in 2022 to just $6 billion in 2024.

The number of deals plummeted from 941 in the first quarter of 2022 to 182 in the first quarter of 2025.

But this part should strike fear into the hearts of every founder claiming “the next big thing” — of the 7,650 companies that raised seed rounds since 2017, only 17% made it to Series A.

And only 1% reach Series C.

This is the maturation of crypto venture investing, and it will be painful for those who thought the party would last forever.

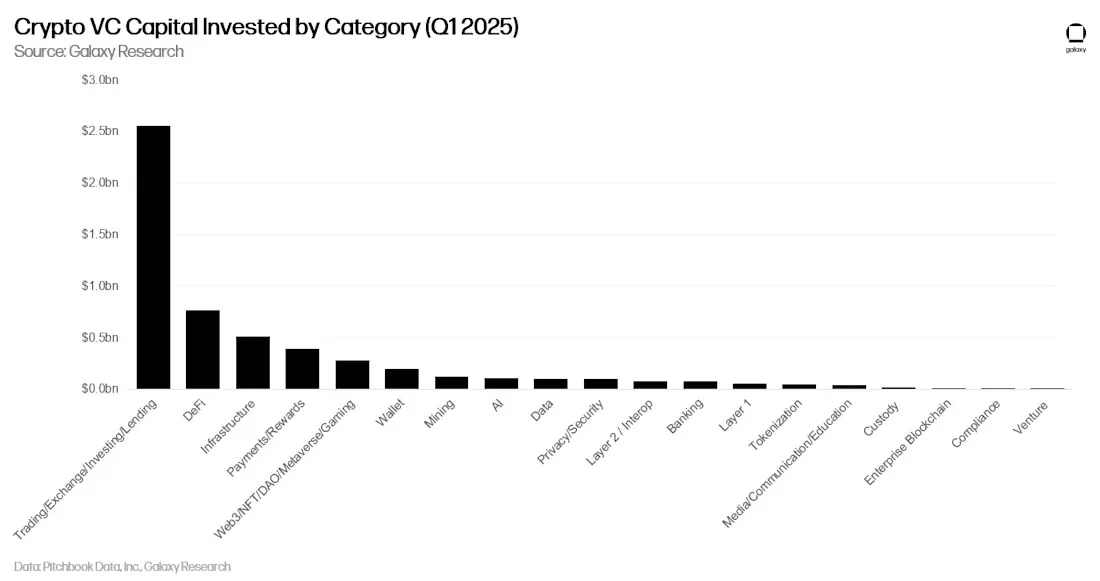

Category rotation

The hot narratives of 2021-2022 — gaming, NFT, DAOs — have all but disappeared from VC interest.

In the first quarter of 2025, companies building transactions and infrastructure attracted the majority of venture capital. DeFi protocols raised $763 million. Meanwhile, the Web3/NFT/DAO/Games category, which once dominated the number of transactions, has slipped to fourth place in capital allocation.

This is VCs finally prioritizing revenue-generating businesses over narrative-driven speculation.

The infrastructure that actually powers cryptocurrency trading is funded.

Apps that people actually use get funded.

Protocols that incur real costs receive funding.

And everything else will become increasingly capital-starved.

Artificial intelligence has also become a major competitor to venture capital.

Why bet on crypto games when you can bet on AI applications with clearer revenue paths? The opportunity cost of crypto-native applications has significantly shifted against projects that cannot demonstrate immediate utility.

Graduation crisis

Let’s dig into the data to find the most sobering statistic: The graduation rate for cryptocurrency from Seed to Series A is 17%.

This means that five out of every six companies that raise a seed round will never receive a meaningful follow-on round.

Compare this to the traditional tech industry where around 25-30% of seed-round companies make it to Series A, and you start to understand the scale of the problem.

The metrics for success in cryptocurrencies have always been fundamentally flawed.

Why? Because for years, the playbook for crypto was simple: raise venture capital, build something that looks innovative, launch a token, and let retail investors provide exit liquidity. VCs didn’t need companies to actually graduate through funding rounds because the public markets would bail them out.

That safety net is gone. Most tokens issued in 2024 are trading at a fraction of their initial valuations. EigenLayer’s EIGEN, which launched at a fully diluted valuation of $6.5 billion, is down 80%. Only a handful of projects are generating more than $1 million in monthly revenue.

When the road to coin listings reaches its end, the true graduation rate gradually emerges. And the results are not optimistic. What is the result? VCs are now asking the same questions that traditional investors have been asking for decades: How do you make money? and When will you make a profit? This is obviously a revolutionary concept in the cryptocurrency field.

Centralized takeover

While the number of deals has dropped significantly, there have been interesting shifts in deal size. The median seed round size has grown significantly since 2022, even though fewer companies are raising money overall.

It’s indicative of an industry consolidating around fewer, bigger bets. The era of “cast-a-net” seed investing is over.

The message to founders is clear: If you’re not in the inner circle, you probably won’t get funded. If you don’t get funding from a top fund, your chances of getting subsequent funding go down dramatically.

This centralization isn’t limited to money.

Data shows that 44% of the companies in A16zs portfolio had A16zs participation in subsequent rounds of financing.

For Blockchain Capital, it’s 25%. The best funds are not only picking winners, they’re actively ensuring their portfolio companies continue to receive funding.

Our View

We have all witnessed the shift from “revolutionary DeFi protocol” to “enterprise blockchain solution”.

Honestly? Im conflicted.

Part of me misses the chaos. The wild swings. The anonymous teams with Discord nicknames raising millions of dollars for ideas that sound like fever dreams.

There is a purity in that madness. It’s just builders and believers betting on a future that traditional finance can’t even imagine.

But another part of me — the part that has seen too many promising projects fail due to insufficient fundamentals — knows that this correction is inevitable.

For years, crypto VC has been operating in a fundamentally wrong way. 스타트업 can raise money based on a white paper alone, launch a token to retail investors to gain liquidity, and then call it a success regardless of whether they have built something that users actually want.

The result? An ecosystem optimized for hype cycles rather than value creation.

Now, the industry is undergoing a long-overdue transition from speculation to substance.

The market is finally starting to apply the performance standards that should have been there from the beginning. When only 17% of seed companies make it to Series A — it means that market efficiency has finally caught up with an industry that was once artificially propped up by over-narratives.

All of this presents both challenges and opportunities. For founders used to raising money based on token potential rather than business fundamentals, the new reality is harsh. You need users, revenue, and a clear path to profitability.

But the environment has never been better for companies building real businesses that solve real problems. Competition for funding has decreased, investors are more focused, and the metrics for success are clearer.

The “tourist money” has left, leaving behind the massive amounts of capital needed for real startups. The institutional investors that remain are not looking for the next “meme coin” or speculative infrastructure investments.

The founders and investors who survive this transition will build the infrastructure for the next chapter of cryptocurrencies. Unlike the last cycle, this one will be built on business fundamentals rather than token mechanics.

The gold rush is over. Mining operations are just beginning.

Although I said miss that chaos? That’s exactly what crypto needs.

This article is sourced from the internet: From enthusiasm to rationality: the maturity of cryptocurrency venture capital

Related: Crypto Shark Effect: How does LBank build a narrative loop in emotional arbitrage?

As Bitcoin broke through the new high of 110,000 US dollars this morning, US President Trump issued a special message to celebrate. A new round of Bitcoin bull market led by institutional funds and long-term capital is accelerating. The market frenzy is no longer just the passionate speculation of retail investors, but a process of sentiment reconstruction and asset repricing driven by macro funds. On May 21, CoinGecko released a list of the Top 10 Cryptocurrency Trading Platforms in the World . In addition to the conventional traditional giants such as Binance, OKX, and Bybit, an unexpected but reasonable name appeared on the list – LBank. This trading platform, which has been working silently on the cold bench for a long time, has gone from being an unpopular marginal player…

还没买