The sequence of events is not complex. The user attempted to swap $50.43 million worth of USDT for AAVE tokens via the Aave frontend interface. The Aave interface displayed a warning for a 99% price impact and required the user to check a confirmation box to proceed. The user checked the box on their mobile phone, and the transaction executed. In the end, they received only 324 AAVE, worth approximately $36,100.

This equates to paying $154,000 per AAVE. The market price was only $111.

Aave founder Stani Kulechov later tweeted his sympathy, promising to refund the approximately $600,000 in frontend fees charged for the transaction and stating they would “look into how to improve these protections.” However, the $50 million loss is a done deal, irreversible on-chain.

This article won’t repeat the headlines you’ve already seen. We aim to trace where this $50 million actually went. Who consumed it within 12 seconds? And why would anyone use $50 million for such an action?

Three Hops, Evaporating Step by Step

This transaction was initiated via the “Collateral Swap” function on the Aave frontend and was routed for execution by a Solver from the CoW Protocol. On-chain data shows the entire transaction was split into three steps.

Step one: The user’s aEthUSDT (interest-bearing USDT receipt) held on Aave V3 was redeemed for 50.43 million USDT. This step was an internal protocol redemption operation; the funds arrived intact with no loss.

Step two: The 50.43 million USDT was pushed into the USDT/WETH pool on Uniswap V3. At the prevailing market price, this amount should have fetched approximately 24,600 WETH. However, because the single order size far exceeded the pool’s liquidity depth, it only actually swapped for 17,958 WETH, worth about $37.07 million. This single step incurred a loss of roughly $13.36 million. These losses were not “deducted” fees but the direct result of price impact. Dumping too much USDT into the pool makes the WETH inside progressively “more expensive”; you buy further down the slippage curve, incurring greater losses. This price difference was passively absorbed by the pool’s liquidity providers (LPs).

Step three: The core of the disaster. The CoW Protocol Solver pushed all 17,958 WETH (worth $37.07 million) into an AAVE/WETH trading pool on SushiSwap. How shallow was this pool? Its total liquidity was only about $73,000.

Dumping $37 million into a $73,000 pool is like trying to pour the entire Pacific Ocean into a swimming pool. The pricing curve of an AMM (Automated 市場 Maker) becomes almost vertical under such extreme ratios. The AAVE tokens in the pool were “bought” at an astronomical price of $154,000 per token, while the market price was only $111.

Ultimately, 17,958 WETH swapped for 331 AAVE, worth about $36,700. The loss in this step was approximately $37.03 million, with a price impact rate of 99.9%. These 331 AAVE were deposited back into Aave V3, minted as aEthAAVE, and delivered to the user.

The entire transaction path can be simply summarized as three hops of progressive evaporation. Hop one: redemption from Aave V3, 50.43 million aEthUSDT became 50.43 million USDT, no loss. Hop two: via Uniswap V3, 50.43 million USDT became 17,958 WETH (worth ~$37.07M), loss ~$13.36M. Hop three: via SushiSwap, 17,958 WETH became 331 AAVE (worth ~$36.7K), loss ~$37.03M. Total loss: $50.39 million. The user ultimately retained $36,100, or 0.07% of the initial capital.

Aave engineer Martin Grabina later clarified a widely misunderstood concept on Twitter. He stated that the core issue was not “slippage” but “price impact.” The quote field on CoW Explorer showed that even before deducting fees and slippage, the raw quote for this transaction was already “50 million USDT for less than 140 AAVE.” This was an extremely poor trade from the outset. The user’s set slippage tolerance of 1.21% was completely meaningless in the face of price impact of this magnitude.

Who Shared the $50 Million Within 12 Seconds?

In the dark forest of DeFi, every on-chain transaction is exposed to everyone, and well-equipped “hunters” are always ready to extract value from any exploitable price imbalance. This transaction perfectly illustrates the complete food chain of Ethereum’s MEV (Maximal Extractable Value) ecosystem.

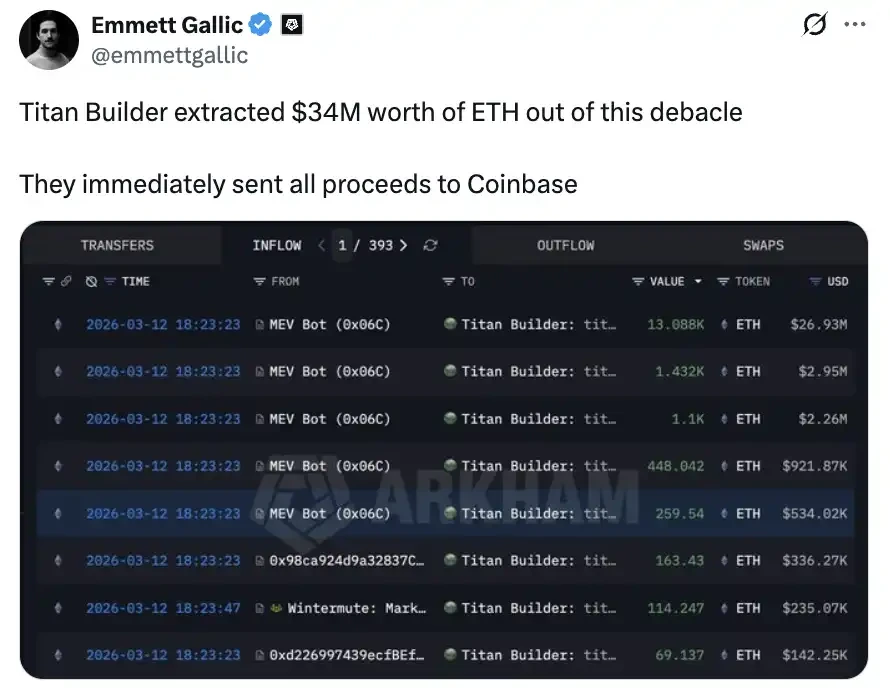

The biggest beneficiary was the Ethereum block builder Titan Builder, taking approximately $34 million. On-chain analyst @emmettgallic tracked that Titan extracted this massive amount of ETH from the block containing this transaction and immediately transferred all proceeds to Coinbase after block confirmation.

To understand the source of these funds, one must first understand Ethereum’s current block construction mechanism. Since Ethereum transitioned to Proof-of-Stake (PoS) and introduced the MEV-Boost system, block production has been split into two roles. Block builders are responsible for assembling transactions within a block and determining their order, while block proposers (validators) are responsible for signing and submitting the block to the chain. Builders compete through bidding; the block with the highest potential profit is more likely to be selected by a validator.

Titan Builder is one of the largest block builders on Ethereum currently, collectively building about 90% of Ethereum blocks with Beaverbuild. In this transaction, Titan’s “God’s eye view” allowed it to perfectly arrange the order of all transactions within the block, maximizing the value extracted from the price distortion. MEV bots, vying for optimal transaction placement, were forced to “bribe” Titan with the vast majority of their arbitrage profits.

The second-largest winners were the MEV searchers, or arbitrage bots, totaling approximately $12 to $12.5 million. These are automated arbitrage programs lurking on the Ethereum chain 24/7, monitoring every pending transaction and striking instantly when they detect exploitable price distortions.

On-chain analyst @CryptoKaleo tracked the most classic MEV arbitrage operation from this incident. An MEV bot executed a risk-free arbitrage of $9.9 million with zero capital within the same block (12 seconds).

The logic of this operation is as follows. The bot first initiated a flash loan from the lending protocol Morpho, instantly borrowing approximately $29 million worth of WETH without any collateral, as long as it was repaid within the same transaction. It then used the borrowed WETH to buy AAVE tokens at the normal market price (~$111 per token) on the Bancor exchange. Next, because the user’s massive trade had pushed the AAVE price in the SushiSwap pool to ~$154,000 per token, the bot sold the AAVE it bought at market price into this distorted pool at an extremely high price, receiving WETH far exceeding its cost. Finally, it repaid the flash loan principal to Morpho, netting $9.9 million. The entire operation was completed within a single transaction, with zero capital input and zero risk.

This is the most brutal aspect of the DeFi “dark forest.” The user’s catastrophic trade created a massive price distortion, and a bot completed the full arbitrage cycle of buying low and selling high within the same 12-second block. Besides this largest arbitrage, other MEV searchers performed similar arbitrage operations during the Uniswap V3 hop as well.

The third layer of beneficiaries were the DEX liquidity providers, gaining approximately $2 to $3.5 million. LPs in the Uniswap V3 and SushiSwap pools, as passive participants, sold tokens to the user at extreme prices via the AMM mechanism. They didn’t need to take any active action; the algorithm automatically priced according to the “the more you buy, the more expensive it gets” curve. The user’s massive order allowed LPs to sell their WETH and AAVE at prices far above market rates.

The fourth layer was Ethereum validators, gaining approximately $1.2 million (~568 ETH). This was the fixed bid paid by Titan Builder to ensure its meticulously constructed “high-profit block” would be selected by the validator on duty for that slot. For the validator, this was just normal block proposal revenue, but significantly more lucrative than an ordinary block.

The final layer was the Aave frontend itself, taking about $600,000. Regardless of how disastrous the trade outcome, the Aave frontend’s routing integration automatically charges a proportional frontend fee. Stani Kulechov has publicly promised to attempt to refund this amount.

Adding these numbers up, the user’s loss of approximately $50.39 million was systematically shared among five layers of the MEV ecosystem within one Ethereum block (12 seconds). The biggest winner was not the bot that discovered the arbitrage opportunity, but the block builder Titan Builder, which controls transaction ordering rights. By collecting “bribes” from bots and directly extracting value from transaction ordering, it monopolized about $34 million, accounting for 67% of the user’s total loss.

This is Ethereum’s “dark forest food chain.” The user creates a price distortion, MEV bots discover and exploit the distortion, bots tribute most of their profits to the block builder, and the builder pays the validator a fee for block inclusion. Layer upon layer of extraction, with clear division of labor, completing the entire profit distribution within 12 seconds.

The Mystery of Motive

As of publication, the identity of the owner of this wallet (0x98B9D979…1FBF97Ac8) remains unknown. But on-chain traces and community analysis leave several clues.

@CryptoKaleo pointed out that this is a brand new wallet address, which received the entire $50.43 million in USDT from Binance 20 days before the transaction occurred. There were no other inbound funds until this catastrophic trade was executed.

Furthermore, this was not an ordinary “buy coins” operation. DeFi analyst YAM noted on Twitter that this transaction used Aave’s Collateral Swap function. The input and output were aEthUSDT and aEthAAVE, respectively—deposit receipts on Aave—not plain USDT and AAVE. This suggests the user likely intended to directly convert their USDT deposit position into an AAVE deposit position within the Aave protocol, rather than simply buying AAVE tokens on the open market.

This leads to the biggest question of the entire incident. The funds came from Binance, where the trading depth for AAVE far exceeds any on-chain DEX. Buying $50 million worth of AAVE on Binance in batches would likely incur slippage of no more than 1-2%. Choosing to withdraw from Binance and then operate on-chain via the Aave frontend was almost the least efficient and most costly method possible.

The community has proposed several speculations. Some believe it could be tax planning. The user might be in a jurisdiction that taxes trades on centralized exchanges but has tax exemptions or weaker tracking for on-chain DeFi operations. By withdrawing from Binance and operating on-chain, they might be attempting to avoid generating taxable transaction records on a CEX.

Other community members speculate it could be an automated trading script or bot that malfunctioned, automatically confirming an anomalous trade without human review. However, this doesn’t explain why the script would check the risk confirmation box. Therefore, it’s more likely a “fat finger” incident. The Aave interface did pop up a 99% price impact warning, but the user confirmed it on their phone. Factors like small-screen mobile operation, habitual dismissal of pop-up warnings, and insufficient understanding of DeFi mechanisms could all have contributed to this disaster.

Looking back, there were ways to avoid disaster at every step of this transaction.

The most basic is order splitting. $50 million should not have been sent as a single transaction. Professional traders use TWAP (Time-Weighted Average Price) strategies, breaking large orders into dozens or even hundreds of smaller trades, dispersing execution across different times and liquidity sources. Even without TWAP, simply splitting it into 50 trades of $1 million each would have reduced the loss by an order of magnitude.

Second is using limit orders. The CoW Swap integrated into the Aave interface supports limit order functionality. If the user had set a reasonable limit price instead of a market order, the trade would have automatically canceled if the ideal price wasn’t met, rather than executing at a disastrous price. Martin Grabina specifically mentioned this point afterward.

Then there’s reading warnings carefully. The interface displayed a 99% price impact warning. This isn’t a routine “Are you sure you want to continue?” pop-up. 99% means you will lose 99% of your funds. Ignoring this number in any transaction is fatal.

Another often-overlooked point is understanding the scale of on-chain liquidity. The AAVE/WETH liquidity on SushiSwap was only $73,000, meaning even a few thousand dollars worth of trading would cause significant price impact, let alone $37 million. Checking the liquidity depth of the target pool is a fundamental step before executing any large DEX trade.

Finally, if one must execute a large on-chain trade, they should use the smart routing features of aggregators like 1inch or Paraswap. These can split orders across multiple liquidity sources, significantly reducing price impact, rather than relying on a single route to push all funds into one shallow pool.

Decentralization gives everyone complete freedom, including the freedom to make irreversible mistakes. In this world with no customer service hotline and no trade undo button, every on-chain click is a final decision.

And the moment you click “confirm,” the hunters in the dark forest have already prepared their flash loans within the same block.

この記事はインターネットから得たものです。 12 Seconds, $50 Million Vanished on Aave

Related: Lazy Investor’s Guide to Wealth Management|Latest Yield Calculation for Binance USD1 エアドロップ; OpenEden Launches New 26.4% APY Pool (January 26th)

Author|Azuma (@azuma_eth) This column aims to cover low-risk yield strategies in the current market primarily focused on stablecoins (and their derivative tokens) (Odaily Note: code risk can never be fully eliminated), to help users who wish to gradually increase their capital size through USD-pegged wealth management find relatively ideal yield opportunities. Past Records 《Lazy Wealth Management Restart|Ethereal Offers 27% APR While Earning Points; Huma Opens New 28% APY Pool (January 6th)》; 《Lazy Wealth Management Guide|Cap’s New Pool APY Climbs After Announcing Stablecoin Airdrop; hyENA Increases LP Quota (January 22nd)》。 交換 Wealth Management The hottest wealth management opportunity at the moment is undoubtedly Binance’s recently renewed USD1 holding subsidy campaign. On January 23rd, Binance announced an airdrop campaign for eligible users holding USD1 on the platform, running from January 23rd to…