The “Plateau” After Hitting New Highs: After $300 Billion, What Are Stablecoins Waiting For?

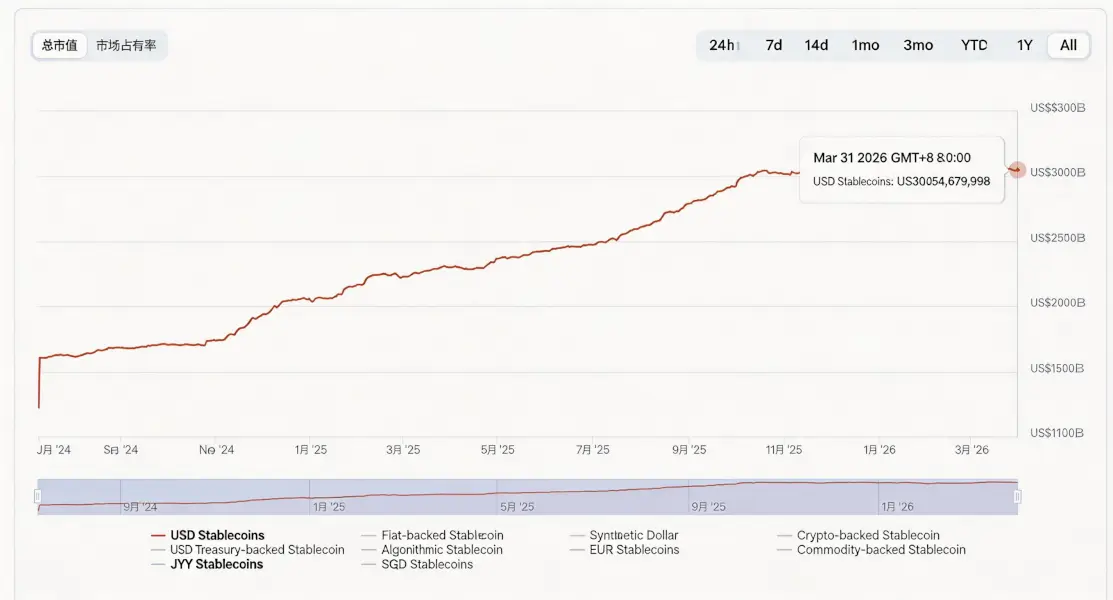

The numbers are impressive, but if you zoom in, you’ll see another side—over the past six months, the growth of stablecoins has begun to vaguely outline a plateau. This isn’t to say the market has lost its imagination, but rather that the logic supporting the scale expansion of the past few years is quietly approaching its own limits.

This means stablecoins need a new narrative, not just new use cases, but deeper attribute changes: When payment scenarios are no longer just about trading, and when the initiators aren’t even human, what role will stablecoins play?

1. The Stuck Ceiling: Change and Constancy

This isn’t the first time stablecoins have reached such a juncture.

From USDT to USDC, to various new types of stablecoins that followed, past rounds of expansion have almost always been accompanied by several familiar scenarios: larger market trading volumes, higher DeFi activity, stronger cross-chain liquidity, and broader global transfer needs.

On the surface, the scale growth of stablecoins comes from supply-side expansion. This isn’t the first time stablecoins have reached such a juncture.

Over the past few years, these core demands have almost entirely originated from human behavior. Whether it’s matching buy/sell orders on exchanges, collateralized lending in DeFi protocols, cross-border transfers and arbitrage paths, or the temporary parking of safe-haven funds, they essentially revolve around the central theme of “trading.” Ultimately, the growth of stablecoins in the previous stage was essentially driven by “human trading demand.”

But the issue today is that while these demands haven’t disappeared, they are increasingly approaching a “predictable ceiling.” After all, the exchange scenario remains vast, but the competitive landscape has become relatively stable; DeFi is still important, but it’s difficult to create explosive incremental growth on its own like in the early days; cross-border payments and arbitrage are still expanding, but it feels more like a process of slow penetration rather than a new narrative capable of reshaping valuation imagination in the short term.

Precisely because of this, market interest in “the next stablecoin system with an incremental growth story” is noticeably rising.

Currently, new increments seem to be concentrated in two main directions.

- One is on-chain yield-bearing stablecoins, which combine stablecoins with structures like government bonds, RWA, and protocol yields, repackaging their appeal through “earning yield just by holding,” similar to the yield-bearing stablecoin path the market has repeatedly discussed in recent years;

- The other, which has become significantly hotter recently, is the on-chain business of AI Agents and the stablecoin payment and settlement needs surrounding it;

Actually, in comparison, the on-chain payment and stablecoin track better fit the characteristics of these new demands because stablecoins naturally possess several conditions that traditional payment systems struggle to combine: 24/7 operation, globally unified settlement, programmability, support for high-frequency micropayments, and no need for complex intermediaries with layer-by-layer authorization.

In other words, what stablecoins are competing for may not just be the existing cross-border payment stock of today, but more likely a larger incremental payment market in the future—especially when the initiators of payments are no longer just human.

2. From Yield-Bearing to AI-Driven: Exploring New Incremental Paths

Recently, traditional giants have clearly been increasing their bets on this latter new direction.

For instance, Visa Crypto Labs launched its first experimental product, Visa CLI, attempting to enable AI agents to securely complete required fee payments when writing code and calling services. If you view this in a broader context, its significance isn’t just about adding another tool, but that the subject of payment is, for the first time, shifting from “human” to “program.”

Because in traditional payment systems, all transactions imply a premise—they must be initiated by a human. Whether it’s bank cards, e-wallets, or mobile payments, they all rely on KYC, manual authorization operations, and finally, the bank account system completes the fund transfer.

Ultimately, the design of this system is essentially built around “human behavior.”

But AI does not belong to this system.

If an AI Agent is to complete a task, it may need to automatically subscribe to data services, pay API fees per call, purchase computing resources across different platforms, or even execute automated trades based on strategies. For such behaviors, waiting for human manual confirmation at every step is neither realistic nor adaptable to its high-frequency, real-time operational rhythm. Moreover, the traditional bank account system wasn’t built for this kind of native interaction between machines.

This is precisely where on-chain payments shine. Stablecoins like USDT and USDC are, in a sense, naturally prepared currencies for AI. They are borderless, programmable, and capable of instantaneous settlement, perfectly matching AI’s pursuit of “high-speed, low-cost, frictionless” operations. This also means that the combination of stablecoins and wallets gives this type of payment true programmability for the first time.

This has given rise to a new form—the “Agent Wallet”—where wallets gradually evolve into AI’s asset interface and execution terminal, manifesting in several typical models in practice (Extended reading: From “Collective Intelligence” to “Super Individual”: How is AI Reshaping DAOs and the Ethereum Ecosystem?):

- Non-Custodial Authorization: You can create an independent, restricted sub-wallet for your AI Agent. It can autonomously trade within limits you set (e.g., single transaction not exceeding 500 USDC) without requiring your manual confirmation each time. The master key remains in your hands, and the AI is merely your authorized agent;

- Cross-Chain Asset Management: AI can query your assets across 100+ chains in real-time and perform rebalancing, staking, or arbitrage based on your set strategies. You are freed from tedious daily monitoring to focus on higher-level strategic decisions;

- Human-Machine Collaboration: This isn’t about complete hands-off management but supports flexible confirmation mechanisms—for instance, automatic for small amounts, alerts for large amounts. AI is responsible for discovering opportunities and constructing trades; you are responsible for the final button press. This model also perfectly combines human judgment with AI’s execution efficiency;

3. From “Who Issues Stablecoins” to “Who Organizes the Network”

If Visa’s experiment represents a change on the demand side, then on the other side, the announcement of the stablecoin mainnet launch by Tempo, a blockchain project backed by Stripe and Paradigm, feels more like an upgrade on the supply side.

Its importance isn’t just that there’s another stablecoin project on the market, but that it reminds everyone once again: The focus of industry competition has long ceased to be just “who can issue stablecoins,” but rather “who can truly organize stablecoins into an operational network.”

Over the past few years, the stablecoin industry first solved the issuance problem.

Mainstream stablecoins like USDT and USDC achieved the scaled supply of on-chain dollars, making “digital dollars” an asset class usable globally for the first time. However, as supply gradually matured, what truly became scarce was no longer the stablecoins themselves, but the ability to connect on-chain accounts, merchant acceptance, corporate payments, and fiat currency clearing networks.

This also explains why, from Stripe to Mastercard, to Visa and PayPal, traditional payment giants have been intensively deploying around stablecoins in the past two years. Even native 加密 platforms have begun to penetrate TradFi in reverse:

- In October 2024, Stripe acquired stablecoin API service provider Bridge for $1.1 billion, setting a new high for M&A value in the 加密 payments field at the time;

- In March of this year, Mastercard acquired stablecoin service provider BVNK for $1.8 billion, breaking that record again;

- Meanwhile, Visa continues to expand its partnership with Bridge, pushing stablecoin-linked cards to a broader market;

- Looking further back, PayPal’s earlier launch of PYUSD also clearly signaled its strategy;

- In the Hong Kong market, licensed compliant exchange OSL announced a shift towards stablecoin payment and settlement infrastructure last year. In January this year, it completed the acquisition of Web3 payment service provider Banxa, and in February, it launched USDGO, a corporate-grade US dollar stablecoin compliant with US federal regulations and distributable in Hong Kong;

Overall, the attitude of the Crypto and broader payments industry towards stablecoins has long shifted from “observation” to “staking a claim.”

This is also why projects like Bridge, BVNK, OSL/USDGO, and today’s projects like Tempo that attempt to build the stablecoin network layer suddenly appear so scarce. Their most valuable aspect lies precisely in their position: connecting on-chain assets and wallets on one end, and merchants, enterprises, payment service providers, and the real-world clearing network on the other.

The industry has moved past the elementary stage of “who issues stablecoins” and entered the second half of “who can make stablecoins truly run.”

In Conclusion

The new high for stablecoins isn’t just a refresh of a scale number; it also resembles a watershed moment.

If the past few years were about stablecoins solving “how humans complete payments on-chain,” then the next question they face is: how to network, scale, and automate the influence of stablecoins?

When AI can autonomously call wallets, when payments are embedded in program execution, when stablecoins become the default settlement currency for global trade, the ceiling for stablecoins will no longer depend solely on today’s market trading volume, nor solely on the speed of replacing existing cross-border payment stock. What it corresponds to might be a larger new variable.

Precisely because of this, what’s truly worth watching in the next round for stablecoins isn’t just whether the supply will continue to hit new highs, but whether it can further evolve into a “global settlement interface.”

And this might be the real driver for stablecoins to break through the plateau of new highs.

本文来源于互联网: The “Plateau” After Hitting New Highs: After $300 Billion, What Are Stablecoins Waiting For?

The crypto space received heavy news today. On March 17, the official Tally X account published a lengthy post, where founder Dennison Bertram candidly stated that the company would officially shut down, and the previously planned ICO was also completely canceled. After more than five years of operation, this team that once provided core infrastructure for decentralized governance has chosen the most honest, yet most difficult, way to exit. Left: CEO Dennison Bertram, Right: CTO Rafael Solari After the X announcement, countless DAO members, developers who once participated in proposals and executed governance through Tally, and those project teams that relied on Tally for stable operation during the bear market left comments like “End of a legend,” “Salute,” and “Heartbroken.” Tally did not fall suddenly; it reached the point where…