Original author: @0x_Arcana

Original translation by Peggy, BlockBeats

Editor’s Note: In the process of gradual digitalization of the global financial system, stablecoins are quietly becoming an undeniable force. They do not belong to banks, money market funds, or the traditional payment system, yet they are reshaping the flow path of the US dollar, challenging the transmission mechanism of monetary policy, and sparking a profound discussion about “financial order.”

This article begins with the historical evolution of “narrow banking,” deeply analyzing how stablecoins replicate this model on-chain, and how the “liquidity black hole effect” impacts the US Treasury market and global financial liquidity. Against the backdrop of incomplete policy and regulatory clarification, the non-cyclical expansion, systemic risks, and macroeconomic impacts of stablecoins are becoming unavoidable new issues for the financial world.

The following is the original text:

Stablecoins revive “narrow banking”

For over a century, monetary reformers have proposed various ideas for “narrow banking”: financial institutions that issue currency but do not provide credit. From the Chicago Plan in the 1930s to the modern Narrow Bank (TNB) proposal, the core idea is to prevent bank runs and systemic risk by requiring currency issuers to hold only safe, liquid assets (such as government bonds).

However, regulators have consistently refused to allow narrow-bank structures to be established.

Why? Because while theoretically safe, narrow-bank lending disrupts the core of the modern banking system—the credit creation mechanism. They withdraw deposits from commercial banks, hoard risk-free collateral, and break the link between short-term liabilities and productive lending.

Ironically, the crypto industry has now “revived” the narrow banking model in the form of fiat-backed stablecoins. Stablecoins behave almost exactly like narrow banking liabilities: they are fully collateralized, instantly redeemable, and primarily backed by US Treasury bonds.

Following a series of bank failures during the Great Depression, economists of the Chicago School proposed a plan to completely separate money creation from credit risk. According to the 1933 “Chicago Plan,” banks were required to hold 100% reserves of demand deposits, and loans could only come from time deposits or equity, not from deposits intended for payments.

The initial intention behind this idea was to eliminate bank runs and reduce the instability of the financial system. This is because if banks cannot use deposits to make loans, they will not collapse due to liquidity mismatch.

In recent years, this concept has resurfaced in the form of “narrow banks.” Narrow banks accept deposits but invest only in safe, short-term government securities, such as Treasury bills or Federal Reserve reserves. A recent example is The Narrow Bank (TNB), which applied for access to the Federal Reserve’s interest on excess reserves (IOER) in 2018 but was rejected. The Federal Reserve was concerned that TNB would become a risk-free, high-yield alternative to deposits, thereby “weakening the transmission mechanism of monetary policy.”

What regulators are really worried about is that if narrow-banks succeed, they could weaken the commercial banking system, drawing deposits from traditional banks and hoarding safe collateral. Essentially, narrow-banks create money-like instruments but do not support credit intermediation.

My personal “conspiracy theory” view is that the modern banking system is essentially a leveraged illusion, operating on the premise that no one is trying to “find an exit.” Narrow banking, on the other hand, threatens this model. But upon closer examination, this isn’t really a conspiracy—it simply reveals the vulnerability of the existing system.

The central bank does not print money directly, but rather indirectly regulates the economy through commercial banks: encouraging or restricting lending, providing support during crises, and maintaining the liquidity of sovereign debt by injecting reserves. In exchange, commercial banks obtain zero-cost liquidity, regulatory leniency, and implicit bailout commitments during crises. Under this structure, traditional commercial banks are not neutral market participants, but rather tools for state intervention in the economy.

Now, imagine a bank saying, “We don’t want leverage; we just want to offer users safe money backed 1:1 by Treasury bonds or Federal Reserve reserves.” This would render the existing fractional-reserve banking model obsolete and directly threaten the existing system.

The Federal Reserve’s rejection of TNB master account applications is a manifestation of this threat. The issue isn’t that TNB will fail, but that it might actually succeed. If people can obtain a currency that is always liquid, free from credit risk, and earns interest, why would they keep their money in traditional banks?

This is where stablecoins came in.

Fiat-backed stablecoins largely replicate the narrow banking model: issuing digital liabilities convertible to US dollars and backing these liabilities 1:1 with secure, liquid off-chain reserves. Like narrow banks, stablecoin issuers do not use these reserves for lending. While issuers like Tether currently do not pay interest to users, this is beyond the scope of this article. This article focuses on the role of stablecoins in the modern monetary structure.

The assets are risk-free, the liabilities are redeemable immediately, and they possess the attributes of face value currency; there is no credit creation, no maturity mismatch, and no leverage.

While narrow-bank systems were stifled in their infancy by regulators, stablecoins have not faced similar restrictions. Many stablecoin issuers operate outside the traditional banking system, and demand for stablecoins continues to grow, particularly in high-inflation countries and emerging markets where access to dollar-denominated banking services is often difficult.

From this perspective, stablecoins have evolved into a kind of “digitally native Eurodollar,” circulating outside the US banking system.

But this raises a crucial question: what impact will stablecoins have on systemic liquidity when they absorb enough U.S. Treasury bonds?

Liquidity Blackhole Thesis

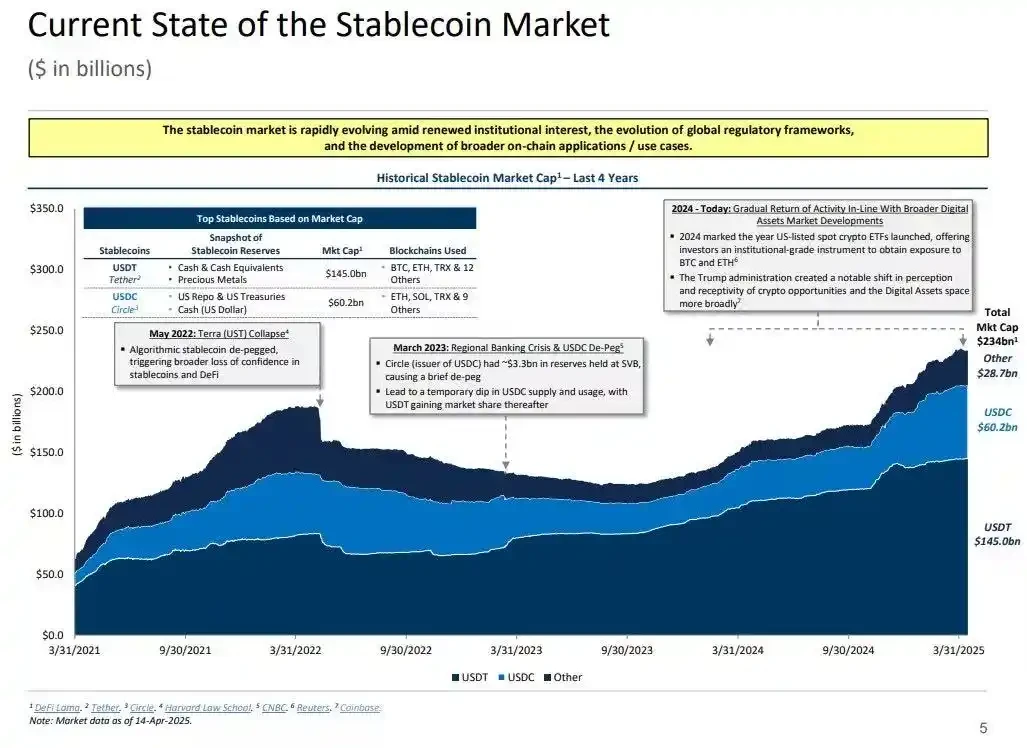

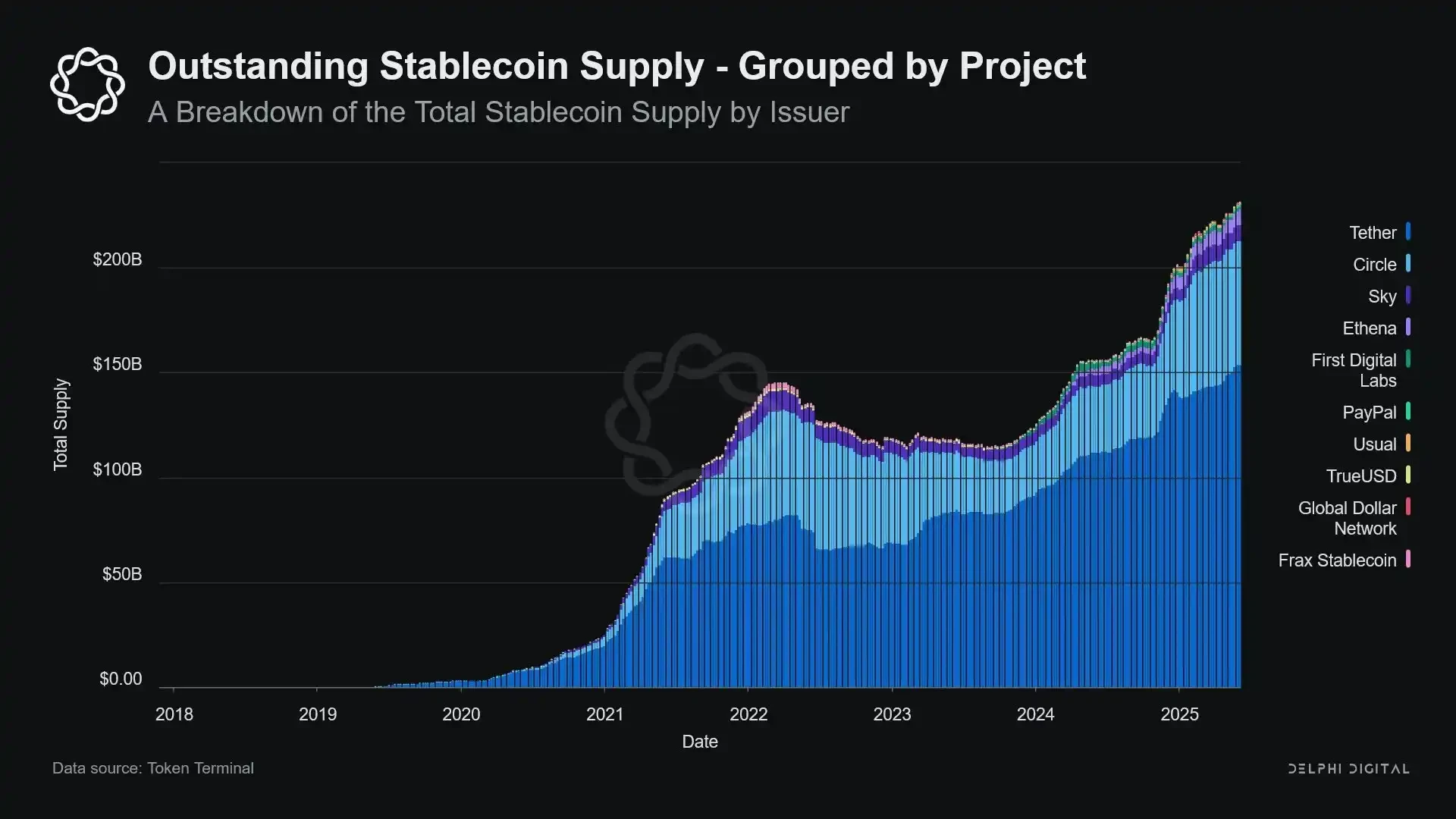

As stablecoins grow in scale, they increasingly resemble global liquidity “islands”: absorbing dollar inflows while locking up secure collateral in a closed loop that cannot re-enter the traditional financial cycle.

This could lead to a “liquidity black hole” in the US Treasury market—that is, a large amount of Treasury bonds are absorbed by the stablecoin system but cannot circulate in the traditional interbank market, thereby affecting the overall liquidity supply of the financial system.

Stablecoin issuers are long-term net buyers of short-term U.S. Treasury securities. For every dollar of stablecoin issued, there must be an equivalent amount of assets backed on the balance sheet—typically Treasury bills or reverse repurchase agreements. However, unlike traditional banks, stablecoin issuers do not sell these Treasury securities for lending or to invest in riskier assets.

As long as the stablecoin remains in circulation, its reserves must be held continuously. Redemption only occurs when a user exits the stablecoin system, which is extremely rare, as on-chain users typically only exchange stablecoins between different tokens or use them as a long-term cash equivalent.

This makes stablecoin issuers one-way liquidity “black holes”: they absorb government bonds but rarely release them. When these government bonds are locked in custodial reserve accounts, they are removed from the traditional collateral cycle—they cannot be re-collateralized or used in the repurchase market, and are effectively removed from the monetary circulation system.

This creates a kind of “monetary sterilization effect.” Just as the Federal Reserve’s quantitative tightening (QT) tightens liquidity by removing high-quality collateral, stablecoins are doing the same thing—but without any policy coordination or macroeconomic objectives.

Even more potentially disruptive is the concept of so-called “shadow quantitative tightening” (Shadow QT) and its persistent feedback loop. It is non-cyclical, does not adjust to macroeconomic conditions, and expands as demand for stablecoins grows. Furthermore, the visibility and coordination of regulation are further hampered by the fact that many stablecoin reserves are held offshore in jurisdictions with lower transparency outside the United States.

Worse still, this mechanism can become procyclical in certain situations. When market risk aversion intensifies, demand for on-chain dollars tends to rise, driving up the issuance of stablecoins and further withdrawing more US Treasury bonds from the market—precisely when the market needs liquidity the most, the black hole effect is amplified.

Although stablecoins are still much smaller in scale than the Federal Reserve’s quantitative tightening (QT), their mechanisms are highly similar and their macroeconomic impacts are almost identical: the amount of government bonds circulating in the market decreases; liquidity tightens; and interest rates face marginal upward pressure.

Moreover, this growth trend has not slowed down; on the contrary, it has accelerated significantly in the past few years.

Policy tension and systemic risk

Stablecoins occupy a unique crossroads: they are neither banks, nor money market funds, nor traditional payment service providers. This ambiguity creates structural tensions for policymakers: too small to be considered a systemic risk and thus subject to regulation; too important to be simply banned; too useful yet too dangerous to thrive unregulated.

A key function of traditional banks is to transmit monetary policy to the real economy. When the Federal Reserve raises interest rates, bank lending tightens, deposit rates adjust, and credit conditions change. However, stablecoin issuers do not lend money, and therefore cannot transmit interest rate changes to the broader credit market. Instead, they absorb high-yield U.S. Treasury bonds, do not offer credit or investment products, and many stablecoins do not even pay interest to holders.

The Federal Reserve’s refusal to allow The Narrow Bank (TNB) access to its master account was not due to concerns about credit risk, but rather to fears of financial disintermediation. The Fed worries that if a risk-free bank offers interest-bearing accounts backed by reserves, it could attract large outflows of funds from commercial banks, potentially damaging the banking system, squeezing credit space, and concentrating monetary power in a “liquidity sterilization vault.”

The systemic risks posed by stablecoins are similar—but this time, they don’t even require approval from the Federal Reserve.

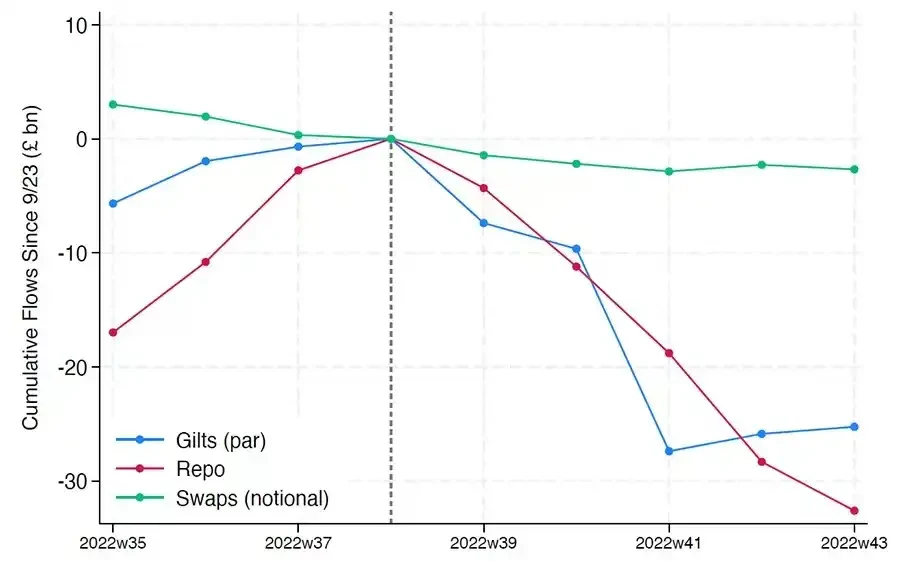

Furthermore, financial disintermediation is not the only risk. Even if stablecoins do not offer yields, the risk of a “run” still exists: once the market loses confidence in the quality of reserves or the regulatory attitude, it could trigger a massive wave of redemptions. In this scenario, issuers may be forced to sell government bonds under market pressure, similar to the 2008 money market fund crisis or the 2022 UK LDI crisis.

Unlike banks, stablecoin issuers do not have a “lender of last resort.” Their shadow banking nature means they can quickly grow into systemic players, but they can also collapse just as quickly.

However, just like Bitcoin, there is a small percentage of cases where the “seed phrase is lost.” In the context of stablecoins, this means that some funds are permanently locked in US Treasury bonds and cannot be redeemed, effectively creating a liquidity black hole.

Stablecoins, initially a peripheral financial product in crypto exchanges, have now become a major channel for dollar liquidity, permeating exchanges, DeFi protocols, and even extending to cross-border remittances and global commercial payments. Stablecoins are no longer peripheral infrastructure; they are gradually becoming the underlying architecture for dollar transactions outside the banking system.

Their growth is “sterilizing” collateral, locking safe assets into cold storage reserves. This is a form of balance sheet contraction occurring outside the control of central banks—an “ambient quantitative tightening.”

While policymakers and the traditional banking system are still struggling to maintain the old order, stablecoins have quietly begun to reshape it.

This article is sourced from the internet: Financial Black Hole: Stablecoins Are Devouring BanksRecommended Articles

Related: Hyperliquid’s old order collapses, DeriW reshapes the future of sustainable DEX

为了止血,Hyperliquid 选择了投票下架合约、统一平仓,这也被社区称为一次赤裸的“拔网线”操作。这也让市场第一次直面残酷现实:在所谓去中心化的外壳下,资金池才是真正的买单者。 当然,Hyperliquid 并非是孤例。GMX 的 GLP 池、dYdX 的保险基金,同样遵循着相似的逻辑,即当清算失效时,亏损最终都会被转嫁给资金池或基金来兜底。表面上,这是一种稳妥的设计,但在极端行情下,它却意味着所有 LP 都要为少数爆仓仓位买单。这也是整个永续 DEX 模式最大的死穴。 当上一代永续合约无法走出性能、去中心化和安全性之间三难困局时,DeriW 给出了另一条答案。 DeriW 的秘密武器 DeriW 是基于 Arbitrum Orbit 构建的新一代永续合约 DEX。与现有行业范式形成鲜明对比的是,它通过 Pendulum AMM(钟摆式动态资金池)与 Layer 3 架构的结合,不仅能够从机制层面切断风险传导,进一步解决了 Hyperliquid 等平台在资金池被动接盘模式下暴露出的一系列顽疾。 同时 DeriW 能够在提供接近中心化交易所的速度与流畅度体验,在保留 DeFi 应有的透明性和非托管属性,同时提供百余种资产的高杠杆交易,以为零 gas 与极低费用的结构,进一步为高频与专业用户打开了大门。 Layer 3 + Pendulum AMM 机制,直击资金池困境 Hyperliquid 的困境揭示了现有模式的本质,即流动性池是所有风险的最终承担者。DeriW 的 Pendulum AMM 机制旨在从源头重构资金池逻辑,同时基于其自研的 Layer 3 架构为此提供性能基础。 风险隔离与定价 Pendulum AMM 的核心创新在于将资金池转化为封闭式基金。每一期认购满额即锁定,存续期内资金不能随意进出,到期后才按份额返还本金和收益。这种制度化的设计让资金池摆脱了随时被抽走的脆弱性,规模稳定、结构可控,LP 的投入回报也更加可预期。 在此基础上,交易规模直接取决于多空双方的净浮动盈亏。博弈越激烈,资金池就能自动扩张,释放超出原始存量的承载力,让有限的资本被压榨到最高效率。与此同时,系统实时监控三大关键参数——头寸净浮动盈亏、资金池的已实现亏损、以及初始资金规模。一旦偏离安全阈值,模型便会自动收紧仓位,并向高风险一方收取额外管理费用,将风险成本切实转嫁回交易者,而非 LP。 更重要的是,Pendulum AMM 通过风险隔离与自动减仓机制,实现了对冲击的局部化处理。即便某个资产池在极端行情中被打爆,风险也被锁定在单一池内,不会演变成平台级的系统性危机。 公平清算 基于上述机制,DeriW 的清算价格由杠杆与保证金共同决定:10 倍杠杆清算率 95%,20 倍 90%,30 倍 85%。仓位一旦触及阈值,系统立即执行清算,优先动用保证金吸收损失,资金池只在极端失衡下才通过滑点被动介入。 这种规则不仅让清算更公平,也极大降低了系统性风险。即便是在“高杠杆+低抵押”的操纵场景下,系统也能依靠费率与阈值的动态调节来拆解冲击,全程无需社区投票或项目方干预。这与 Hyperliquid 在 JELLY 事件中的“拔网线”操作形成了鲜明对比,凸显了 DeriW 的去中心化公正性。 与此同时,DeriW 所有交易和清算数据均能在 Layer 3 上透明执行,并最终提交至 Ethereum,继承其安全性与数据可用性。用户不仅完全掌控资产,还可以随时验证链上数据,甚至通过 Layer 1 的欺诈证明机制发起挑战。这样的透明度与抗审查性,让系统免于黑箱操作和单点控制。 Layer 3 性能所带来的极致体验 任何复杂的机制都需要性能作支撑。DeriW 基于 Arbitrum Orbit 构建的 Layer 3,不仅支持 80,000 TPS 的吞吐量和零 Gas 成本,还确保即便在极端行情下,清算也能即时落地。对用户而言,这意味着在 DeFi 中获得接近中心化交易所的速度与流畅度,同时保留公开透明与非托管的安全属性。 值得一提的是,DeriW 由老牌交易所 CoinW 开发,团队在永续合约领域已有八年经验,并通过 CertiK 审计。这一背景为平台的稳定性和可信度提供了现实背书,也成为其获得市场信任的前置条件。 交易效率的降维打击 传统订单簿模式的缺陷不断显露: 流动性不足时,挂单迟迟不成交,延迟与滑点横行; 高频交易者难以跑出策略,小额用户则不断被隐性成本蚕食。 DeriW 通过 Pendulum AMM 搭配自研 Layer 3 ,能够在去中心化且公开透明的前提下,让整个过程保持接近 CEX 的速度与流畅度。 在成本上,其直接将资金费率设定为零,市场平衡由 AMM 内置的动态滑点来承担,只有在多空严重失衡时才会触发。手续费则固定为 0.01%,处于行业最低档。相比动辄 0.02%–0.05% 的主流平台,这种低费率和零资金费率的组合,显著降低了长期持仓与高频交易的摩擦成本。 效率与成本的叠加优势,正在让…