Trading Everything, Never Closing: RWA Perpetual Contracts — The Final Piece for DeFi to Devour Wall Street (Part 1)

Foreword:

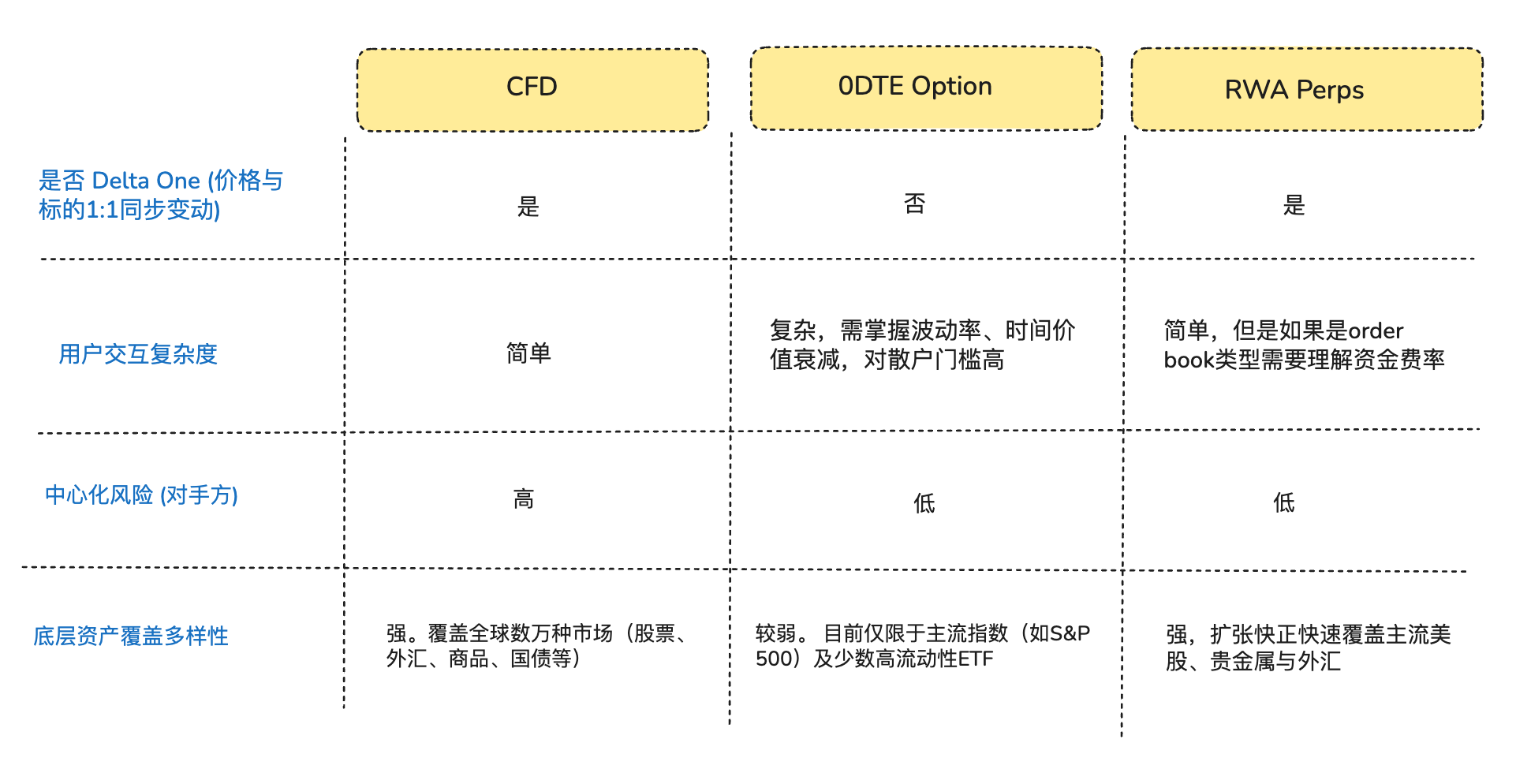

In fact, the true engine of liquidity in global financial markets is not the static holders of assets, but traders seeking leveraged directional exposure. From the U.S. end-of-month options market with a notional value of approximately $50 trillion to the non-U.S. CFD (Contract for Difference) market with a monthly trading volume of about $30 trillion, retail investors’ thirst for high-leverage, short-term risk exposure has never ceased. Despite the enormous trading scale, existing traditional financial instruments still struggle to adequately bear this demand: 0DTE Options (Zero Days to Expiration/End-of-Day Options) force traders to bear not only directional bets but also the nonlinear risks of Theta (time decay) and Vega (volatility). Meanwhile, the CFD market is often criticized for its opaque black-box mechanisms and centralized counterparty risks.

From the perspective of traders seeking purely directional exposure, what many traders truly crave is not “options” or “tokenized stocks,” but a pure Delta One (linear/symmetric payoff) exposure—where fluctuations in asset prices are directly and proportionally converted into investment gains or losses without any intermediate decay or deviation (Arthur Hayes wrote an article titled“Adapt or Die” at the end of last year reviewing the complete background of their development of kripto perpetual contracts, which is an interesting read)..

It is within this structural mismatch that DeFi protocols have keenly captured this market opportunity. Some DeFi entrepreneurs are attempting to introduce perpetual contracts, which have been validated and matured over nearly a decade in the Crypto market, into the realm of traditional assets. These products adopt a synthetic derivatives architecture, anchoring the price of underlying assets through oracle price feeds and funding rate mechanisms, providing round-the-clock leveraged trading services for stocks, commodities, and forex without the need to physically hold or deliver the assets.

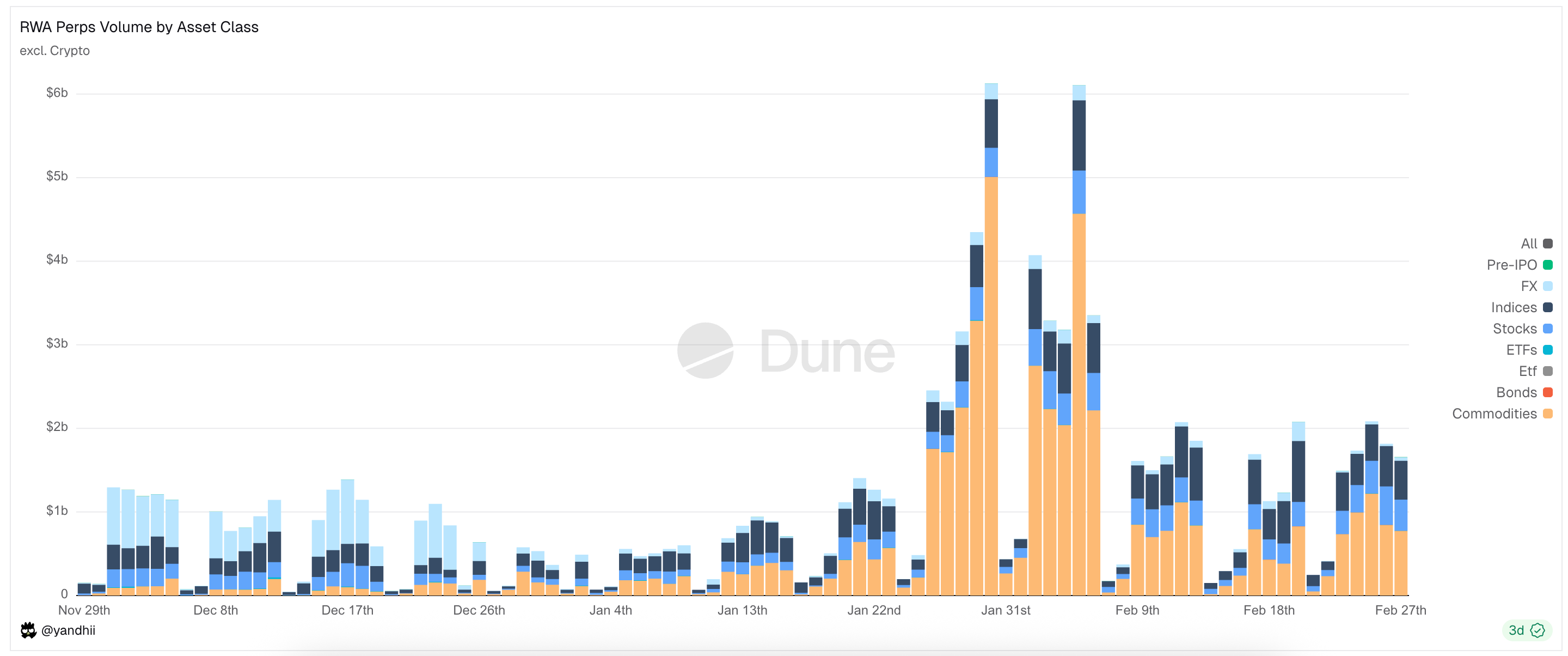

Figure: Main asset types currently traded on RWA Perps Dex

1. Pasar Background (The Entry Opportunity for the RWA Perps Market)

1.1 Target Market 1: The U.S. 0DTE Option (End-of-Day Options) Market

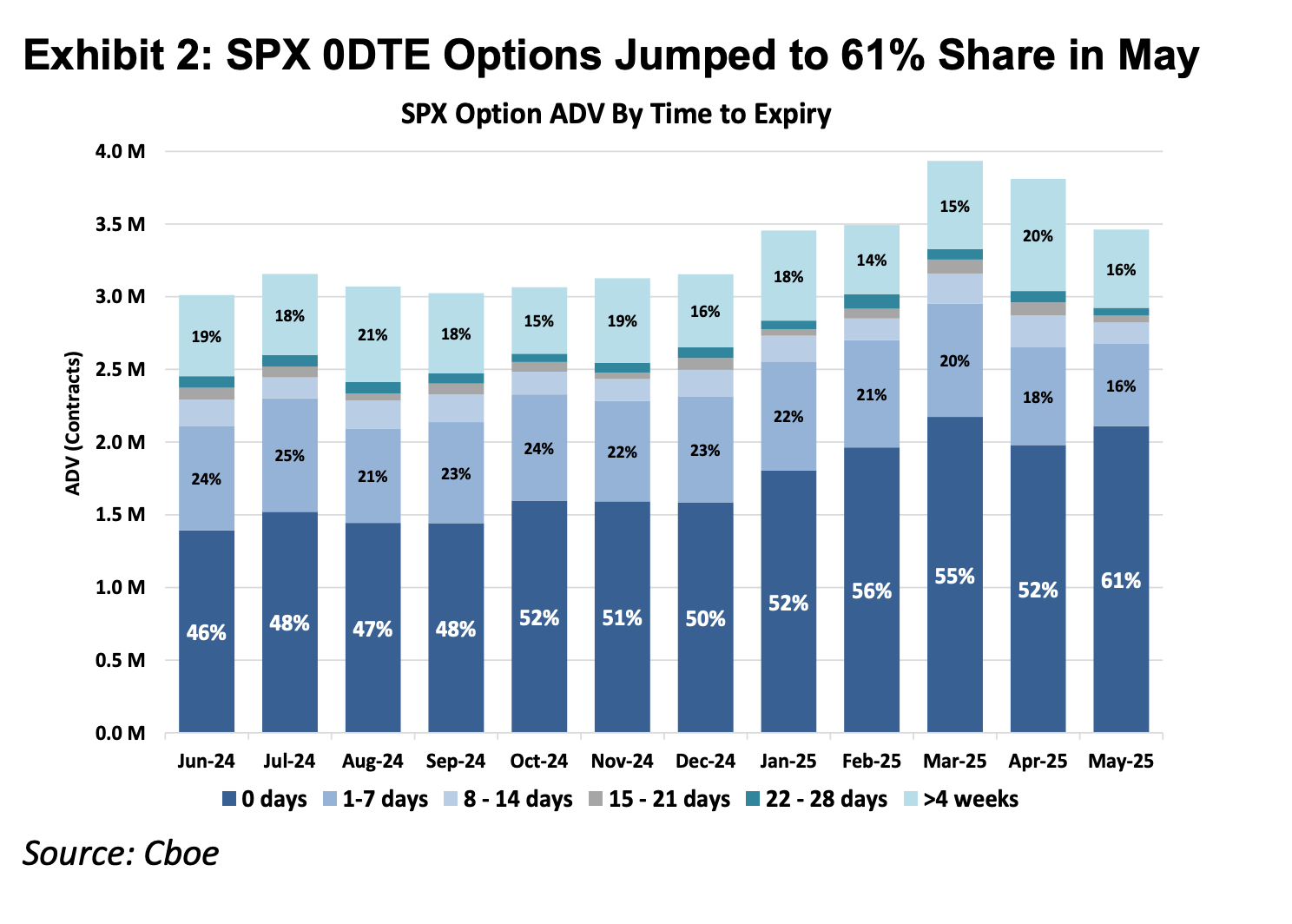

The U.S. options market has undergone a profound structural transformation over the past decade. According to data from the major options exchange Cboe Global Markets, the trading volume share of end-of-day options in S&P 500 index options has surged from less than 5% in 2016 to over 60% currently, with a monthly notional trading volume of $48 trillion (approximately 40 times the monthly trading volume of CEX perpetual contracts). This data not only reflects an increase in trading frequency but also reveals the existence of a massive force of capital seeking extremely high intraday leveraged exposure.

Note: 0DTE stands for “Zero Days to Expiration,” meaning options that expire on the same trading day, also known as end-of-day options. These contracts expire at the end of the trading day. Traders use them for ultra-short-term speculation to obtain quick returns and avoid overnight holding risks.

Figure: The two charts above show the proportion of S&P 500 index options with different expiration times from 2016 to 2025. It can be seen that 0DTE Options accounted for only about 5% of the options market in 2016, but their market share soared to 61% by 2025. This indicates that nearly half of S&P 500 index option trades are betting on intraday direction for ultra-short-term speculation.

Figure: The chart above shows that retail investors are the absolute main force in the 0DTE market.

From the first principles of financial instruments, financial derivatives can be divided into Delta One products and non-linear products. Traditional Delta One instruments like stocks and futures have symmetric risk exposure: the gains from a rise in the underlying price and the losses from a fall are linearly proportional in scale. However, options were originally designed to manage asymmetric risk.

For example, a fund manager holding a large amount of Apple stock, bullish on the company’s long-term fundamentals and unwilling to sell, might worry about short-term earnings volatility causing a sharp price drop. In this case, they could buy put options to insure their position. Under this structure, their profit potential is preserved as the stock price rises (symmetric upside), but their loss is strictly capped at the premium paid (asymmetric downside).

It is precisely to achieve this “separation of rights and obligations” insurance function that the cost structure of an option must include not only the intrinsic value (Delta) reflecting direction but also the time value (Theta) reflecting the possibility of volatility (Gamma) and the passage of time.

The significant growth in the share of the 0DTE market in recent years reveals a paradox: a large number of traders are not using it to manage asymmetric risk or conduct complex volatility trading, but rather as the only means to obtain intraday directional leverage. In this scenario, traders are forced to pay the expensive cost of time value (Theta Decay) for an “insurance function” they do not need. As long as the underlying asset’s rise is insufficient to cover the decay of time value, even with correct directional judgment, trades can still result in losses.

Figure: Time value is the main component of an option that decays over time and is also the core battleground for 0DTE option traders.

Therefore, as a Delta One product, the value of perpetual contracts lies in stripping away the extraneous costs of time and volatility, providing pure linear leveraged exposure. From a mathematical logic perspective, they can more precisely match the speculative needs of this portion of capital compared to 0DTE Options.

1.2 Target Market 2: The Non-U.S. CFD Market

In markets outside the U.S., retail leverage demand is primarily met by CFDs (Contracts for Difference). In 2025, the average monthly trading volume of the CFD market reached $30 trillion.

Although CFDs offer a linear payoff Delta One structure, their market operation model is based on a broker model, presenting significant transparency issues. The vast majority of CFD brokers adopt a B-Book (internal market making) model, meaning the broker acts directly as the counterparty to the client (within the industry, there are also risk-conscious brokers who hedge against profitable clients to avoid risk. However, as the top few companies in the CFD market account for only about 20% of market share, the remaining 80% is filled with numerous small and medium-sized brokers. Overall, there is no shortage of brokers relying on opaque black-box operations and profiting from client losses). In this zero-sum game structure and opaque black box, brokers possess the technical authority and economic incentive to modify quotes, slippage, and execution speeds.

Compared to CFD products, RWA Perps can also be understood as a form of “transparent, smart contract-based CFD.” By putting clearing logic, funding rate calculations, and oracle quotes on-chain, DeFi protocols eliminate the possibility of centralized brokers interfering with trading outcomes. Simultaneously, the atomic settlement mechanism based on stablecoins elevates capital transfer efficiency to the second level, achieving true self-custody of funds and real-time clearing.

2. Product Construction Challenges for RWA Perps

RWA Perps are not simply replicating the Perps we have seen focused on crypto assets. Crypto assets possess characteristics like 7×24 trading, real-time pricing, and T+0 on-chain settlement, but traditional assets are constrained by the legal frameworks of the physical world, holiday systems, and outdated bank clearing protocols.

This asynchronicity in underlying attributes constitutes the “impossible triangle” in RWA Perps product design:

- High Leverage: Meets retail users’ speculative demand for high-multiple leverage.

- 24/7 Availability: Maintains the core value proposition of DeFi for trading anytime, anywhere.

- Risk Externalization: Ensures the protocol and market makers do not bear directional betting risks, enabling systemic long-term survival.

2.1 How are RWA Perps On-Chain Prices Anchored When the U.S. Stock Market is Closed?

The essence of Perps products is a “mirror of price discovery,” requiring a continuous external spot price feed. However, when Nasdaq or CME closes on weekends and overnight, it creates a break in the oracle data source.

This pricing vacuum and dislocation during U.S. stock market closures give rise to two core risks:

Risk 1: Lack of Sufficient Risk Hedging Channels for Market Makers During Weekend Closures

Professional market makers can provide extremely narrow spreads and deep liquidity because they do not bet on direction but seek neutral positions, only collecting spreads. This means that for every $1 million worth of Tesla stock contracts a market maker sells to traders on-chain, they must immediately buy an equivalent amount of the asset in traditional spot or futures markets to hedge that risk exposure.

When traditional markets are closed and hedging channels are shut, market makers cannot adjust their hedge positions. To avoid this risk, market makers can only choose to withdraw orders or add massive risk premiums to their quotes during closure periods. This explains why traditional order book models see spreads nonlinearly expand to dozens of times their normal levels on weekends, easily leading to liquidity drying up.

Risk 2: “Gap Risk” from Extremely High or Low Opening Prices on Monday

Due to the 24/7 nature of crypto-native asset trading, asset price curves are typically continuous, giving liquidation engines sufficient time to close user positions as prices fall. However, in the RWA Perps domain, the accumulated upward or downward pressure on traditional assets during closures is released instantaneously at Monday’s open. If there is a significant gap opening on Monday, the liquidation engine finds itself in a vacuum during this “price discontinuity,” unable to find counterparties to execute liquidations before positions become undercollateralized.

To address these dilemmas, current RWA Perps platforms have two main approaches:

- Internal Simulated Pricing (e.g., TradeXYZ / Hyperliquid): Introduce an Exponential Moving Average (EMA) algorithm to allow prices to slowly “drift” based on on-chain buy/sell pressure when the oracle is disconnected, maintaining a 7×24 facade, but theoretically remaining a potentially manipulable “shadow market.”

- Forced Risk Downgrade (e.g., Ostium): This is a more pragmatic risk control solution. Ostium introduces a 0DTE-like property: requiring all high-leverage positions to be automatically closed or significantly deleveraged before the market close. Only low-leverage positions (with sufficient margin buffer to cover 5%-10% gaps) are allowed to be held overnight. This approach sacrifices some “perpetual” nature in exchange for absolute system safety against Monday gap openings, preventing the LP pool from being penetrated by systemic bad debt.

2.2 How to Provide TradFi-Level Trading Depth On-Chain at Low Cost?

In DEX development, the choice of liquidity supply and order execution mechanism is a core variable determining system capital efficiency, risk distribution logic, and user experience. The two mainstream solutions currently are: CLOB (Central Limit Order Book) and Oracle-based Pool.

Hyperliquid validated the success of the order book model for crypto-native assets, with its core advantage being frictionless hedging execution: market makers can transfer risk across platforms in milliseconds using stablecoins. After taking orders on the on-chain order book, market makers can hedge risk on 7×24 CEXs in milliseconds using stablecoins. Since crypto funds and assets operate within a highly interconnected crypto network, hedging costs are extremely low, allowing market makers to compress quoted spreads to very narrow ranges, thereby attracting trading volume and forming a positive feedback loop.

In the RWA domain, market makers face significant cross-border hedging friction: On one hand, the time mismatch between on-chain USDC (T+0) and traditional fiat settlement forces market makers to keep large amounts of idle USD in traditional accounts as hedging reserves. On the other hand, the closure of traditional banks on weekends and holidays means market makers cannot hedge promptly during non-business hours in the face of sudden market movements.

This is also the core logic behind why founders like Kaledora of Ostium insist on pursuing a pool-based model rather than an order book. She believes that the frictionless hedging seen in crypto-native asset exchanges is difficult to achieve in the RWA perps domain. When a market maker takes an NVDA order on an RWA Perps platform, they cannot use stablecoins to hedge on Nasdaq in milliseconds because they must overcome numerous obstacles across traditional banking channels.

2.3 How Does the System Ensure Its Own Solvency When Traders Continuously Profit from One-Sided Market Trends?

The third dilemma involves how the protocol ensures long-term solvency through external hedging. The pool model of GMX has been able to survive long-term in the crypto market because it acts as a “passive house,” leveraging statistical advantages under large sample sizes to steadily absorb the holding wear and tear and liquidation profits generated by high-leverage positions amid frequent volatility. In the crypto market characterized by significant oscillation, the mathematical expectation of this model is favorable for pool LPs.

But the risk distribution of RWA assets is completely different. Mainstream indices like the S&P 500 often experience sustained, one-sided bull trends lasting several years. In the absence of a risk externalization (hedging) mechanism, users’ continuous profits would directly translate into net losses for the LP pool, causing the system not only to fail to capture volatility premiums but to be completely drained by one-sided positions, ultimately facing solvency exhaustion.

3. Representative Projects and Architectural Battles: Oracle Pricing + Pool (Pool based + Oracle pricing) vs. Order Book (Order book)

Artikel ini bersumber dari internet: Trading Everything, Never Closing: RWA Perpetual Contracts — The Final Piece for DeFi to Devour Wall Street (Part 1)

Related: tetesan udara Weekly Report|ETHGas to Conduct Airdrop Snapshot on January 19; Solana Mobile Opens Airdrop Claims on January 21

Author | Golem (@web3_golem) Odaily has compiled a list of airdrop projects available for claiming from January 12 to January 18, 2026, along with key airdrop news during this period. For detailed information, please refer to the main text. Solana Mobile Project and Airdrop Eligibility Introduction Solana Mobile is a hardware device developer supported by Solana, having launched the web3 mobile device Seeker. The project announced the opening of the SKR airdrop check on January 15. This airdrop distributes nearly 2 billion SKR tokens in total to the community, with approximately 1.82 billion allocated to 100,908 users and about 141 million allocated to 188 developers, covering both user and developer groups. Users can directly check their token allocation on their phones. Officials stated that SKR will officially open for claiming…