Non-Fragmented Positions: Hands-On with Hyperliquid HIP-4, Trading “Events” as Spot Assets

A trader stared at the screen, juggling three layers of judgment in their mind: they believed weekend war news would escalate, and the probability of BTC dipping first then rising was underestimated; they thought the outcome of the next Fed meeting wasn’t fully priced in; they also wanted to buy weekend gap insurance for their crude oil or precious metals positions.

The trouble was, these three tasks used to require three different venues. Placing long/short bets on a futures exchange, wagering on events on a prediction market, and hedging on an options exchange, with margin split three ways. The insight was holistic, but the positions were fragmented.

Hyperliquid’s new market framework, HIP-4, addresses this fragmentation.

What is HIP-4?

HIP-4 transforms “outcomes” themselves into tradable, standardized assets. It allows judgments like “whether an event will happen” or “whether a price will reach a certain level by a specific time” to enter Hyperliquid’s trading system as standardized assets. It launched on Hyperliquid’s testnet on February 2nd.

A community member recently reverse-engineered the core contracts of HIP-4 based on the deployed contract bytecode on the testnet, giving us a glimpse of its architecture before the mainnet launch.

HIP-4 frontend simulated by the community based on testnet contracts

HIP-4 frontend simulated by the community based on testnet contracts

HIP-4 employs a dual-layer structure. Trading occurs on HyperCore, while fund custody, prize pool management, and partial settlement happen on HyperEVM. The former handles high-frequency order matching, the latter manages the more complex contract logic of prediction markets. The division of labor is clear.

Through HIP-4, abstract “events” can be “transposed” into genuinely tradable assets.

Suppose someone creates a market for “Who will win the 100-meter dash” with event ID 9, where outcome 0 represents “Hypurr wins.” This outcome would be mapped to the “#90” token on HyperCore, traded on an order book. Traders buy and sell it just like a spot asset.

For markets similar to options, like “Will BTC touch a certain price within 15 minutes?”, settlement at expiry is based on real-time price data directly on HyperCore, eliminating the need for external oracles.

The settlement rules for event contracts like “Who will win the 100-meter dash” are not yet fully clear.

Overlapping User Profile with Polymarket

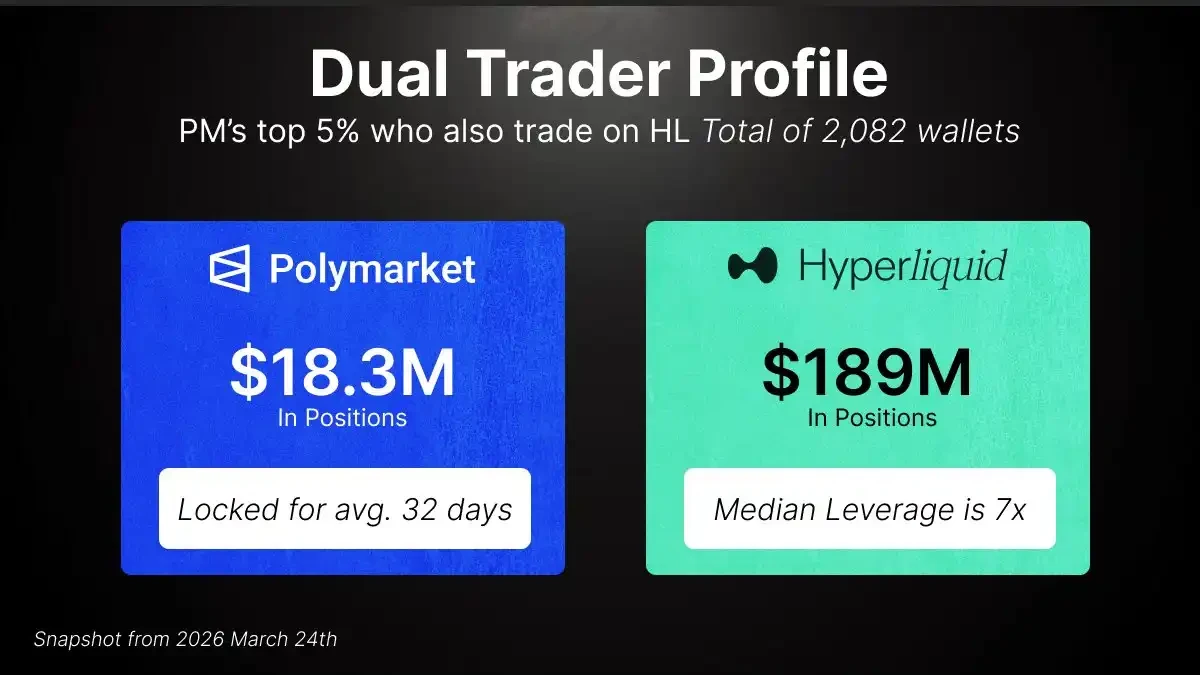

A study analyzing nearly 15,000 active Polymarket addresses found that among top traders, a group was already active on Hyperliquid.

This overlapping user group contributed approximately $1.43 billion in trading volume on Polymarket, while simultaneously managing a total of about $189 million in perpetual contract positions on Hyperliquid, with margin usage around $29 million. These addresses’ Hyperliquid accounts showed a near-balanced long/short distribution, primarily trading mainstream assets like BTC and ETH. On Polymarket, they tended to hold positions on longer-cycle events like elections and Fed decisions. This clearly indicates a group of typical sophisticated traders.

Today, these two sets of positions reside in two isolated systems. Approximately $18.3 million in prediction market holdings cannot be integrated into the perpetual contract margin system. Based on these overlapping users’ average leverage of about 7x on Hyperliquid, this theoretically corresponds to over $120 million in additional trading capacity.

Targeting TradFi’s Weak Spots, New Imagination for On-Chain Finance

The greater potential of HIP-4 lies in its composability.

The community has already outlined several types of potential new products:

Weekend Gap Options: Traditional markets have a long gap between Friday’s close and Sunday’s open. HIP-4 could directly turn this gap into a weekend gap option. A trader holding crude oil, silver, or stock-related positions in HIP-3 (perpetuals), worried about a sudden gap before Monday’s open, could buy an option that pays out based on the difference between Friday’s close and Sunday’s open price for hedging.

Internal/External Price Deviation: Payouts based on the maximum deviation between HIP-3’s internal pricing and external oracle prices, hedging against liquidation risk.

Funding Rate Options: Allowing traders to hedge against negative funding rates.

These structured instruments are precisely what differentiate HIP-4 from traditional prediction markets. The latter often lacks natural counterparties, with markets dominated by insider traders who continuously harvest uninformed retail traders and market makers.

In contrast, HIP-4’s structured products have inherent hedging demand, not just serving a gambling function. The pricing logic of market makers, liquidity quality, and market depth would all reach another level.

Insight has never been linear, and positions shouldn’t be either.

With the same account, the same margin, and the same settlement system, HIP-4 brings Hyperliquid one step closer to its vision of a “House of All Finance.”

यह लेख इंटरनेट से लिया गया है: Non-Fragmented Positions: Hands-On with Hyperliquid HIP-4, Trading “Events” as Spot Assets

Related: BTC’s “Narrative Crisis”: Bloomberg Is Right, But Only Half Right

No crash, no black swan event, no exchange or project running away with funds. It’s just that feeling of being slowly bled dry. A little drop each day, another little drop the next. Over a trillion dollars in market cap has evaporated, yet there hasn’t even been a decent news story about it. Right at this moment, on February 21st, Bloomberg published an article titled “Bitcoin’s Trillion-Dollar Identity Crisis Is Coming From All Sides.” Its core argument can be summarized in three sentences: Gold is stealing the macro hedge narrative, stablecoins are stealing the payment narrative, and prediction markets are stealing the speculation narrative. In my view, Bloomberg got two-thirds of it right, but they missed the most crucial third. Some Data You Can’t Argue With Content creators often fall…