AI Infrastructure Surged Throughout Q1; Who Can Sustain “High Valuations” in Q2?

Previously, MSX published an overview outlook titled “Soaring Oil Prices, Stubborn Rates, and the ‘Seven Sisters’ Stalling: Which Themes Should Drive Excess Returns in Q2 US Stocks?“, which systematically outlined the overall market themes for Q2. Delving deeper into this framework reveals that the Q1 AI rally in US stocks is far more complex than simply “whether the leading computing power stocks will rise.”

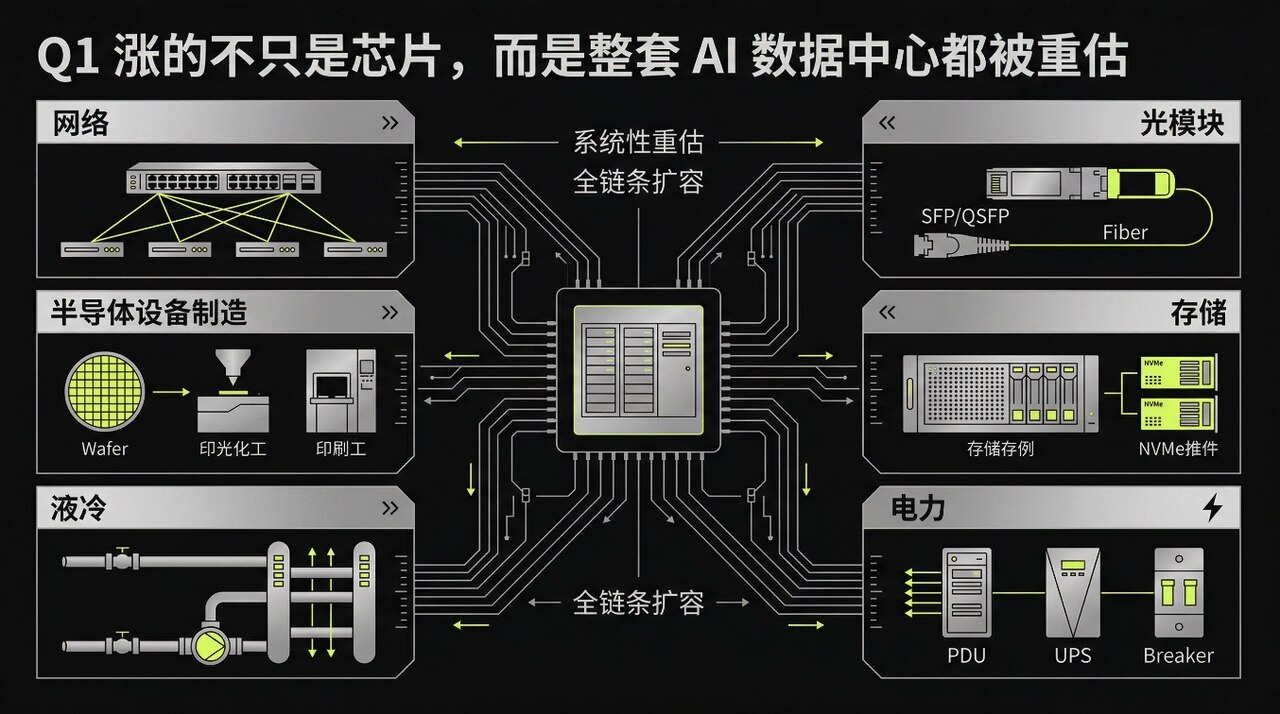

From the perspective of MSX Research, it’s not just a few companies around GPUs that are rising, but the entire data center ecosystem: expanding facilities, increasing bandwidth, supplementing power supply, deploying liquid cooling, and pushing production capacity forward.

Therefore, entering Q2, the main theme remains unchanged, but the market rhythm will shift.

Networking, optics, storage, power, and equipment manufacturing are still on the main theme, but the subsequent trend will not be a simple, uniform valuation lift across the entire “AI infrastructure” chain. Instead, it will depend more on whether orders, deliveries, profits, and capex can meet expectations.

Looking at performance within the period, AEHR.M and AAOI.M have shown the strongest momentum since Q2 began. On a Year-to-Date (YTD) basis, AAOI.M, SNDK.M, AEHR.M, and LITE.M have seen more pronounced gains, clearly indicating that significant divergence has already emerged within the AI infrastructure chain.

1. What Was Bought in Q1 Wasn’t a Single Company, But the Entire Data Center Needing Expansion

The most notable aspect of the Q1 rally is that, as it progressed, capital was no longer solely focused on individual chipmakers. Chips are still the entry point, but the real capital expenditure (capex) sink is the entire data center. As long as hyperscalers continue to increase their capex, money will flow down the chain based on “what’s still missing for AI implementation.”

Looking at the asset pool on the MSX platform, this theme already has a relatively clear trading mapping.

Networking was the first to strengthen. AI clusters are not about single-machine computing power contests; they compete on interconnectivity, bandwidth, and latency. Switch leaders like ANET.M naturally lead the charge. Companies like CRDO.M, MRVL.M, focusing on critical interconnect and accelerator peripherals, and names like AVGO.M, which hold positions in both chips and connectivity, are also lifted by the market. While CIEN.M is more on the periphery of network infrastructure, as long as cross-facility transmission and data movement volumes increase, it’s hard to completely bypass. Once clusters scale up, networking is no longer a supporting role but a legitimate expense item.

Next is optics. As AI training and inference move towards higher density, optical modules and related components are increasingly brought to the forefront. LITE.M, COHR.M, AAOI.M, and FN.M were repeatedly grouped together in Q1. The logic is straightforward: bandwidth needs to increase, interconnects need upgrading, and specifications need to move higher. In the initial phase, the market wasn’t in a hurry to pick winners and losers; it first lifted the valuation for the “specification upgrade” narrative itself. Questions about who is at 800G, who is at 1.6T, and who can capture higher-end shipments were temporarily set aside.

Storage was also re-categorized. MU.M, WDC.M, STX.M, and SNDK.M were traditionally viewed more as cyclical stocks. However, in the Q1 market, capital began pushing them towards the “AI infrastructure chain.” The reason is clear: larger models, more data, and more frequent training mean memory and storage are no longer just following the old PC and smartphone logic. At least from a trading perspective, the market is now willing to re-evaluate these companies within the “data center expansion” framework.

Following that are power and thermal management. Typical beneficiaries like VRT.M (“power supply + cabinets + supporting equipment”) and names more focused on power equipment and grid infrastructure like GEV.M may not have been in the hottest spotlight every day in Q1, but they were also lifted by capital. After all, you can pack computing power into a facility, but questions about where the power comes from, how to dissipate heat, and whether delivery can keep up all need to be accounted for. Once data center density increases, none of these issues can be avoided.

Equipment manufacturing hasn’t fallen behind either. The line of LRCX.M, KLAC.M, AMAT.M, MKSI.M, TER.M, TSEM.M, and AEHR.M benefited more in Q1 from the expectation that “capacity expansion will continue to propagate downstream.” Advanced processes, storage, packaging and testing, yield management, production line automation, and testing/validation—once the market places these segments within the “next stage of AI capacity expansion” framework, valuations shift upward accordingly.

So, the Q1 rally wasn’t about one or two companies surging alone; it was the entire chain being lifted together. The market first settled on one thing: data centers need to expand. Subsequently, networking, optics, storage, power, thermal management, and equipment manufacturing were all put on the table.

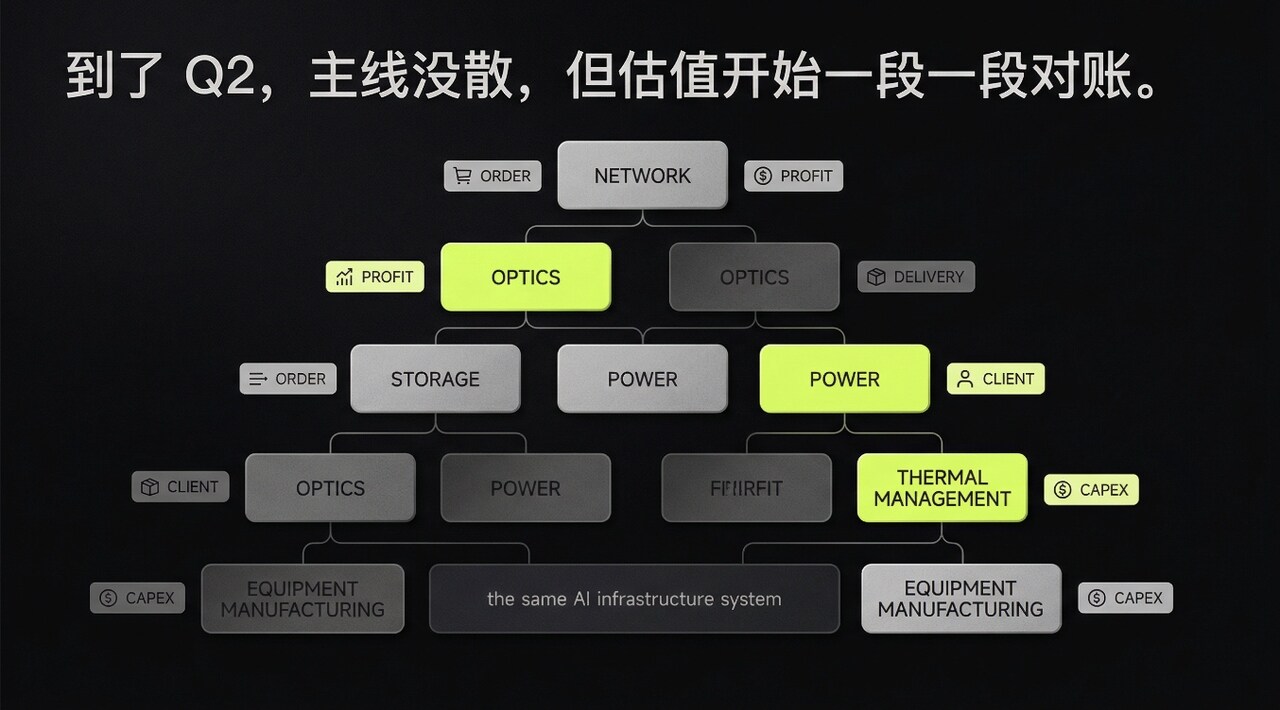

2. Entering Q2, the Main Theme Remains, But Valuation Starts Being Scrutinized Segment by Segment

The issue in Q2 isn’t that the AI narrative has suddenly vanished, but that the first round of “uniform valuation lift across the entire chain” has already played out. There will still be gains, but they won’t be as synchronized as before.

The networking and optics chains in Q1 benefited from expectations of high bandwidth, interconnect upgrades, and cluster expansion. In Q2, these expectations won’t disappear but will be broken down and scrutinized. Names with clearer customer bases and more stable product cycles like ANET.M will be watched to see if order strength can persist. Companies at critical junctures around interconnects and computing power like CRDO.M, MRVL.M, and AVGO.M will face market questions about customer mix, shipment cadence, and revenue recognition. Names more focused on network infrastructure like CIEN.M will be judged more on new orders, delivery cycles, and project progress in Q2, unlikely to continue riding the entire chain’s premium.

The optics chain is more prone to divergence. Because even with the same specification upgrade narrative, the underlying customers, capacity, yields, and pricing pressures differ. LITE.M, COHR.M, AAOI.M, and FN.M could rise together initially. In Q2, the market will scrutinize them one by one: whose customers are more stable, whose shipments are smoother, whose profits can be retained. The first phase relied on “buying the optics chain as a group”; the next phase focuses on who can deliver on the numbers.

The storage side might be more complicated. In Q1, the market was willing to give MU.M, WDC.M, STX.M, and SNDK.M a more “AI-like” valuation. In Q2, it will start asking: how solid is this demand wave, can profit recovery keep pace, or is this just another cyclical rebound in a new guise? As long as prices, bit shipments, and profits move up together, capital will continue to assign valuation. But if the financials aren’t strong enough, the pullback will be direct. The biggest fear for the storage line is being bought as AI infrastructure only to be re-categorized as cyclical stocks.

Power, thermal management, and equipment manufacturing might actually be easier to evaluate on fundamentals in Q2. They may not be in the hottest discussions daily, but when it comes to checking the numbers, delivery, capacity expansion, order visibility, and gross margin trends are clearer. The order and delivery cadence of VRT.M and the broader power equipment cycle where GEV.M sits will be compared against hyperscalers’ expansion plans. On the equipment manufacturing side, the line of LRCX.M, KLAC.M, AMAT.M, MKSI.M, TER.M, TSEM.M, and AEHR.M will also be watched: can AI capacity expansion truly propagate downstream, can testing/validation, production line cadence, and final delivery keep up, or will it stall at the initial upstream investments?

The first phase was buying by sector as a group; the next phase requires looking at companies one by one. The main theme remains, but valuations won’t move in lockstep anymore.

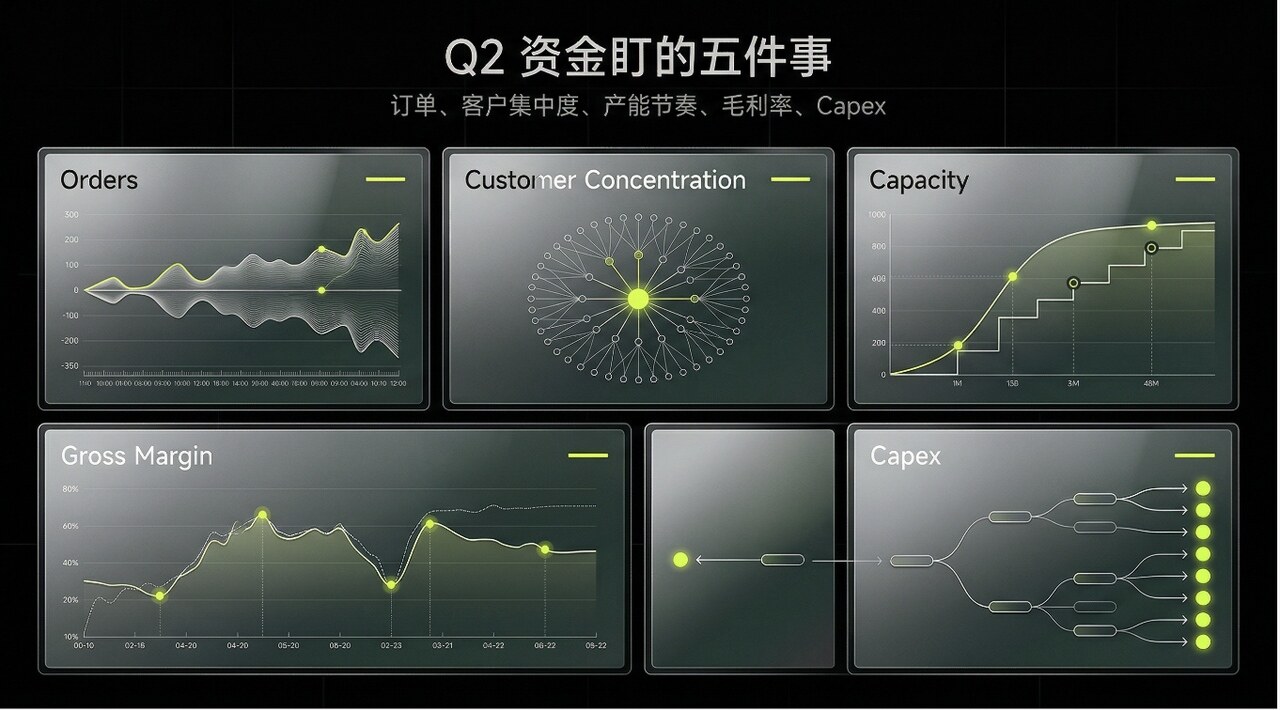

3. The Five Things Q2 Capital is Watching: Nailing High Expectations to Financial Statements

First, look at orders. The networking chain is often the first to be scrutinized: are orders still piling up, is delivery accelerating, are customer purchases moving from trial orders to regular procurement. Typical beneficiaries like ANET.M will be repeatedly questioned on whether order strength can persist. Companies at critical interconnect and computing power peripherals like CRDO.M, MRVL.M, and AVGO.M will also be watched for more visible projects and clearer shipment guidance.

Second, look at customer concentration. The optics chain can’t avoid this issue. Higher concentration often meant faster gains in Q1; in Q2, if a major customer slows down, the stock price often reacts ahead of the earnings report. For the group of LITE.M, COHR.M, AAOI.M, and FN.M, the market will care more about who the customers are, their proportion, and their cadence, rather than smoothing out

This article is sourced from the internet: AI Infrastructure Surged Throughout Q1; Who Can Sustain “High Valuations” in Q2?

Author|Azuma (@azuma_eth) The threat of quantum computing to cryptocurrencies has once again become a focal point of discussion on international platforms. The so-called “quantum threat” refers to the possibility that sufficiently powerful quantum computers in the future could break the cryptographic foundations that currently secure cryptocurrencies, potentially destroying their security models. In November last year, when Vitalik discussed the quantum threat at the Devconnect conference, Odaily published an article titled “Is the Quantum Threat Resurfacing, Shaking the Foundation of Cryptocurrencies?”. The core argument of that article was that while the quantum threat objectively exists, first, there is still some time before a real threat materializes; and second, cryptocurrencies can be upgraded to incorporate post-quantum algorithms, thereby completing a “lock change”. In other words, it was a matter of “worthy of…