When is the crypto industry most profitable, yet also most fearful?

Original Compilation: Saoirse, Foresight News

The kripto market’s Fear and Greed Index has hit a historic low. Yet, at the same time, the industry’s profitability has reached unprecedented heights.

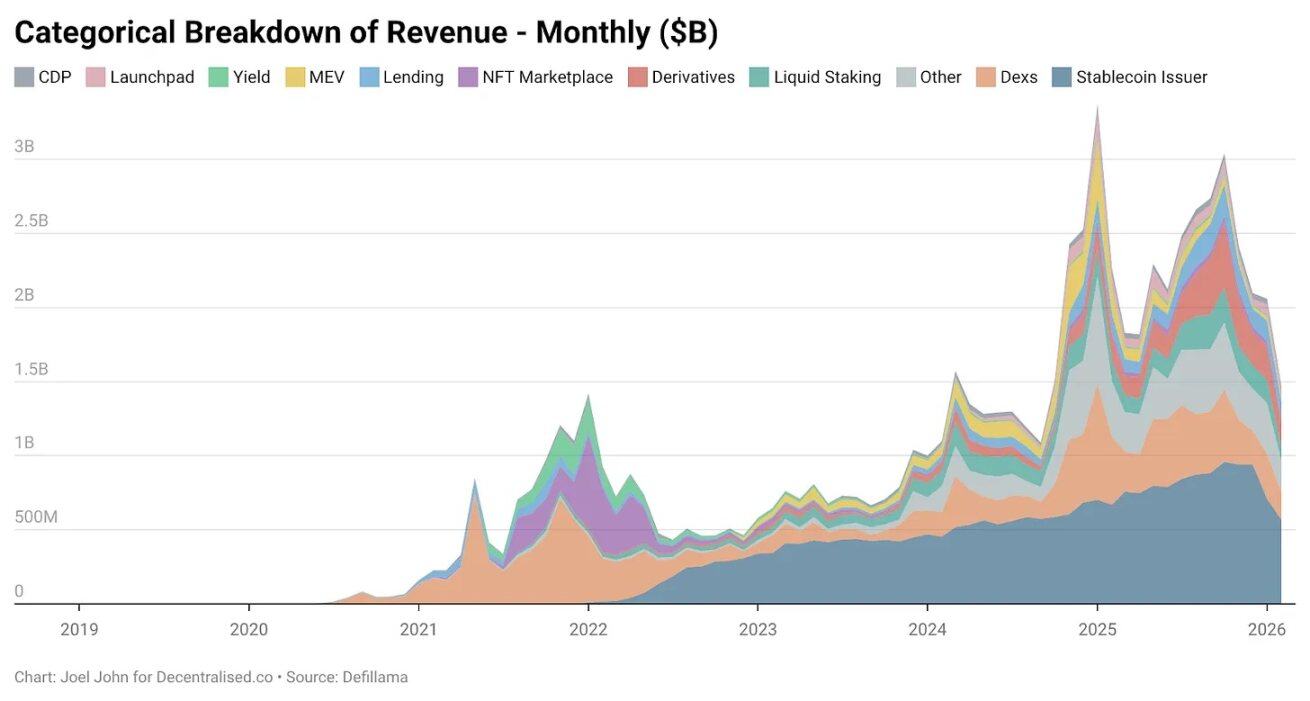

Since 2018, DeFiLlama data shows that crypto-native protocols have cumulatively generated $74.8 billion in fees. Nearly half of that — $31.4 billion — was created in the 18 months from January 2024 to June 2025.

Why is there still so much fear when an industry is having its best quarters in eight years?

In the past two months, 12 projects have shut down directly: Entropy Protocol, Milkyway Protocol, Nifty Gateway, Rodeo, Forgotten Runiverse, Slingshot, Polynomial, Zerolend, Grix Finance, Parsec Finance, Angle Protocol, Step Finance. These are products built by passionate entrepreneurs we respect, who persevered for years.

OKX, Mantra, Polygon Labs, Gemini, and Binance have also conducted layoffs. Conference attendance is down, VCs are pivoting to AI, developers are flocking to AI. The pessimism in the industry is real. “If you’re in crypto, switch to AI fast” has become the mainstream sentiment.

But should you really switch? We’ve been pondering this question for the past few weeks.

When a new technology emerges, the market initially assigns it a massive premium due to its novelty and grand vision. In the 19th century, nearly 6% of the UK’s GDP was invested in railway stocks. In 2026, hyperscale cloud providers’ capital expenditures will account for 2% of US GDP.

But when reality sets in, technology valuations return to rationality.

What truly matters is: during this return to normalcy, can the industry prove itself useful?

In this article, I will break down:

- How the crypto industry’s revenue has evolved;

- How sticky the generated capital is;

- What the industry’s true moats are.

Ledger Study: A Dramatic Shift in the Revenue Landscape

Crypto-native businesses have been making money since the industry’s inception.

Menukarkans like Bitmex, Binance, and Coinbase have long been immensely profitable. But they are centralized, held by a few, and their revenues are not public.

DeFi-native protocols like Uniswap and Aave changed all that. You can verify daily how much a protocol actually earns. Token valuations should reflect the economic activity supported by these foundational components.

Until 2022, decentralized exchanges still accounted for 28.4% of the industry’s total revenue, generating $2.27 billion that year. The lending sector was also highly concentrated: Aave and Compound took 82% of lending fees. Back then, people believed: sectors have leaders, but long-tail protocols also have room to grow. The technology itself was novel enough to support high valuations.

Then came the phase of crypto’s expansion to the masses.

NFT once represented a hopeful vision: cultural value priced on-chain. Celebrities changed their Twitter avatars, ordinary people thought this would lead to mass adoption. OpenSea generated $1.55 billion in revenue that year, capturing 71.7% of the NFT market.

In hindsight, its $13 billion valuation didn’t seem outrageous — it could have become a long-term monopolist.

But fate and the market had other plans.

By 2025, NFT revenue accounted for less than 1%. We experienced a bubble akin to “Beanie Babies,” but in the end, we didn’t even have physical souvenirs left.

(Note: Beanie Babies were a series of plush toys launched by the American company Ty (founded by Ty Warner) in 1993, and were also a famous global collecting craze and speculative bubble case in the mid-to-late 1990s.)

In contrast, decentralized exchange revenue grew, but valuations plummeted. Last year, DEXs generated $5.03 billion in fees, lending platforms $1.65 billion. Combined, they accounted for 22.9% of total fees, far below the 33.1% in 2022. Their share of economic activity shrank within a larger pie, and their valuations contracted even more drastically.

So what is growing?

How has the crypto-native business model evolved from 2022 to today? The answer lies in the data:

In January 2026, stablecoin issuers Tether and Circle took 34.3% of the entire industry’s fees. In other words: for every $1 the industry earns, 34 cents goes into the pockets of these two companies. Their revenue doubled from $4.95 billion at the beginning of 2023 to $9.89 billion in 2025, almost entirely from US Treasury yields.

This is a bank-level financial product, yet growing at a startup’s pace. Tether’s revenue is almost three times that of Circle.

Their rise stems from two forces:

- Demand

The Global South has long needed tools to hedge against local inflation and transfer funds freely. The US dollar, even a digital one, fills this gap — something local currencies cannot. Capital flight is a necessity, not an add-on feature.

- Cost Structure

Blockchain handles the operational aspects of the stablecoin business. Unlike traditional banks or fintech companies, Tether and Circle don’t need to hire proportionally as issuance scales. Issuing another $1 billion on-chain or transferring $100 billion between addresses has near-zero marginal cost.

Demand pulls, costs are pushed to the extreme. The combination makes stablecoin issuance one of the most capital-efficient businesses in financial history.

The moat for stablecoins lies in: liquidity, compliance, and the time advantage. Very few issuers survive multiple cycles.

Tether and Circle take nearly 99% of stablecoin issuance revenue. Why? Because they started early. The network effects from integration across multiple exchanges create a legitimacy that technology alone cannot achieve. Tether initially launched on the Omni sidechain, slow and clunky, but it was accessible in OTC desks and exchange touchpoints.

This is a distribution barrier, not a technological one. This is a moat that crypto-native entrepreneurs relying solely on code find hard to replicate.

New Growth Engine: The Explosion of Trading-Focused Applications

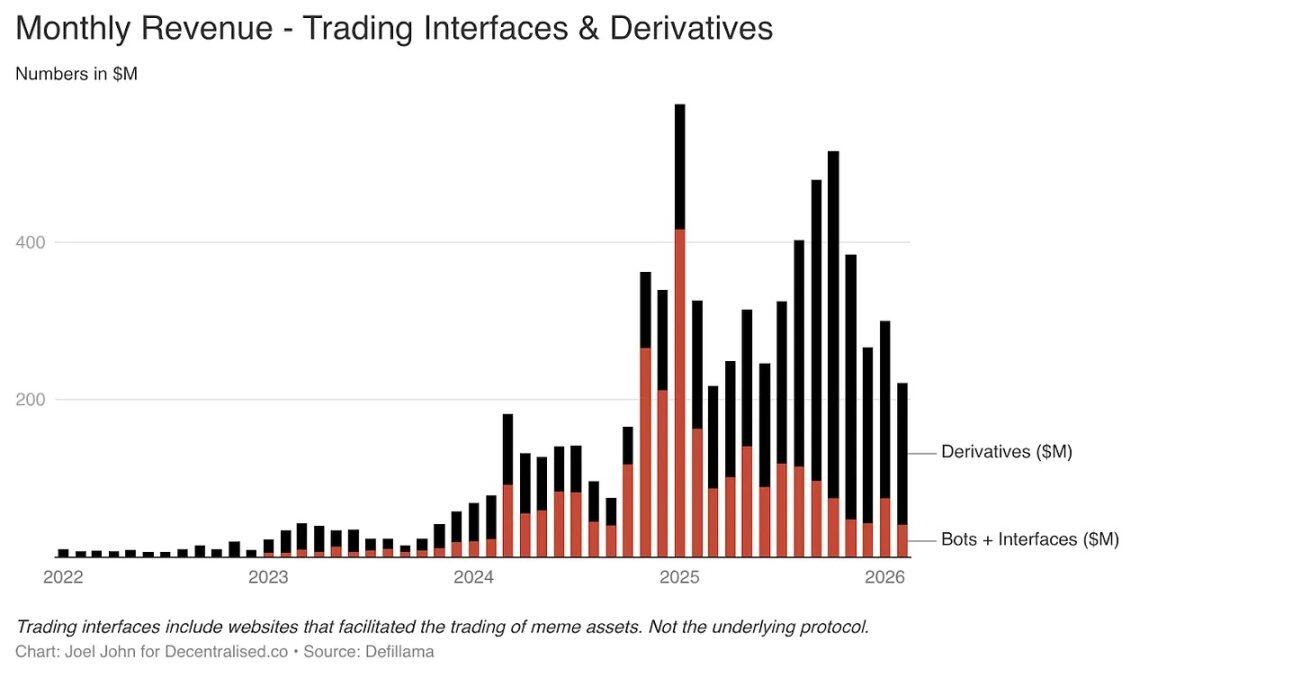

We mentioned in a previous article: crypto is essentially a trading economy. But we didn’t anticipate back then that products based on Telegram trading bots and trading interfaces would grow this fast.

In January 2025, these two sectors alone generated $575 million in monthly fees. The reason is simple: this is what users actually want.

Meme coin trading and perpetual futures exchanges allow users to profit quickly. In pursuit of high returns, they are willing to pay high fees.

From 2022 to 2025, this sector’s share of total revenue soared from 1% to over 15%.

Products like TryFomo and Moonshot, focusing on end-users, have made millions. Technically not complex, the key is: aggregating and packaging crypto-native foundational components to create a better user experience. With tools like Privy maturing, developers no longer need to incentivize liquidity or worry about wallet management. The foundational components we were excited about in 2022 are now mature. Applications like BullX and Photon are built on top of them.

From January 2024 to February 2026, this sector created $1.93 billion in fees. But meme assets have a fatal flaw: they are lightweight applications with extreme seasonality.

Does this sound familiar?

NFTs and Web3 games also experienced similar explosions, then collapses. This cyclicality is both a bug and a feature of the industry.

Perpetual futures exchanges (and later, prediction markets) represent a more durable new direction.

PumpFun democratized asset issuance through meme coins, but the game wasn’t fair. Eventually, the market sobered up: meme coins die.

The dream of getting rich overnight by buying a funny token shattered. People don’t want to manage a bunch of random tokens; they want exposure.

Perpetual futures provide that.

You can trade Bitcoin, Solana, Ethereum with high leverage. Pasar makers and traders seeking alternatives to centralized channels flocked in. The core of this category is liquidity.

Hyperliquid became the leader because its order book depth rivals that of centralized exchanges. Without that parity of experience, users have no reason to migrate. Over the past three years, Hyperliquid and Jupiter have taken the majority of fees in this sector.

Perpetual futures exchanges and trading platforms tear off the industry’s fig leaf: the real way to make money is by taking small fees from high-frequency trading. Meme trading platforms and perpetual exchanges are “dopamine machines” that package and sell risk. Some of them will mature into core financial infrastructure — used globally in the future to trade commodities, stocks, and digital assets even on weekends.

Blockchain-native applications have replicated what Robinhood and Binance already provided: a channel for risk.

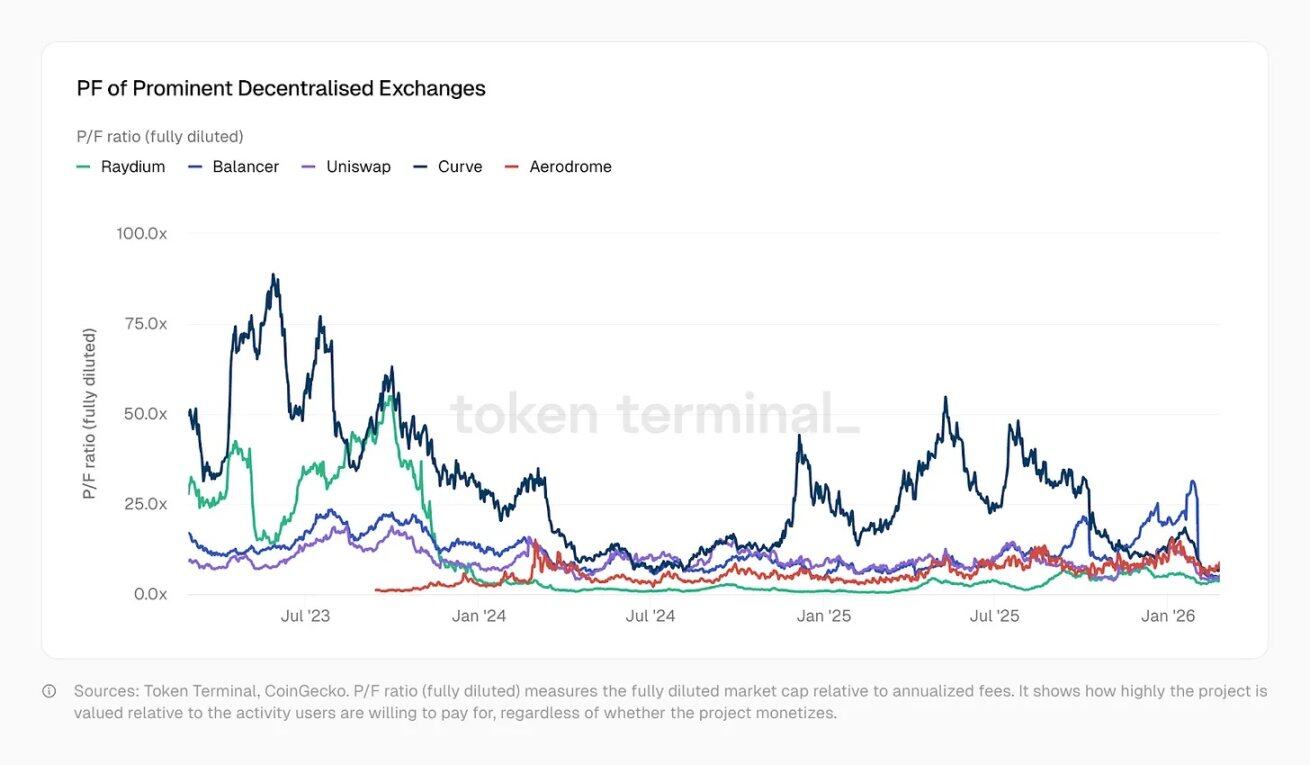

Hungry Fat Protocols: Public Chains and DeFi Valuations Plunge

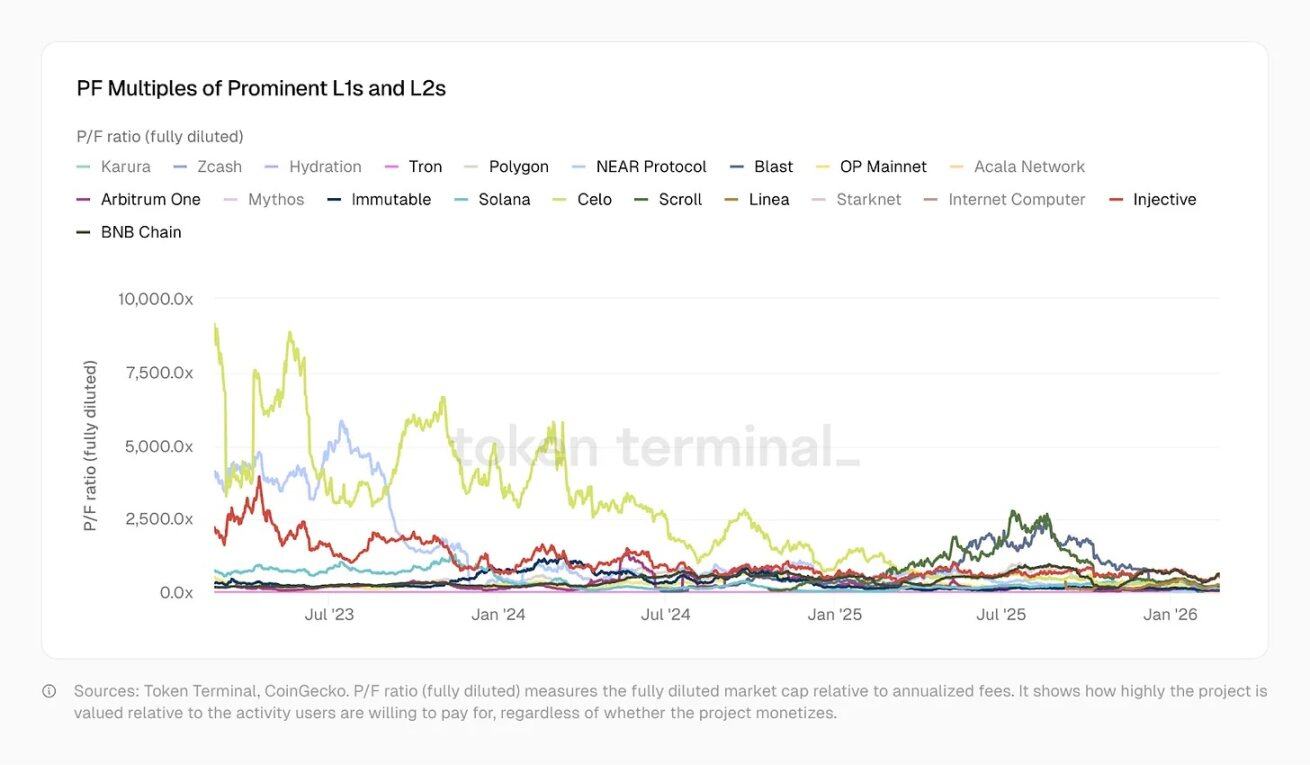

So far, I haven’t mentioned the underlying public chains. Because their story is completely different: they are victims of the novelty premium and are now moving towards a discount.

January 2023:

- Optimism Price-to-Fees (PF) ratio: 465x

- Solana: 706x

- Arbitrum, BNB: ~206x

Today:

- Solana: 138x

- Arbitrum: 62x

- OP: 37x

- Polygon: only 20x, approaching traditional fintech companies

- Tron, supporting the stablecoin ecosystem, is only 10.2x

These public chains have supported more complex products over these years, with more users, better liquidity, and richer financial applications. Yet their Price-to-Fees ratios have fallen sharply, reflecting a shift in market sentiment.

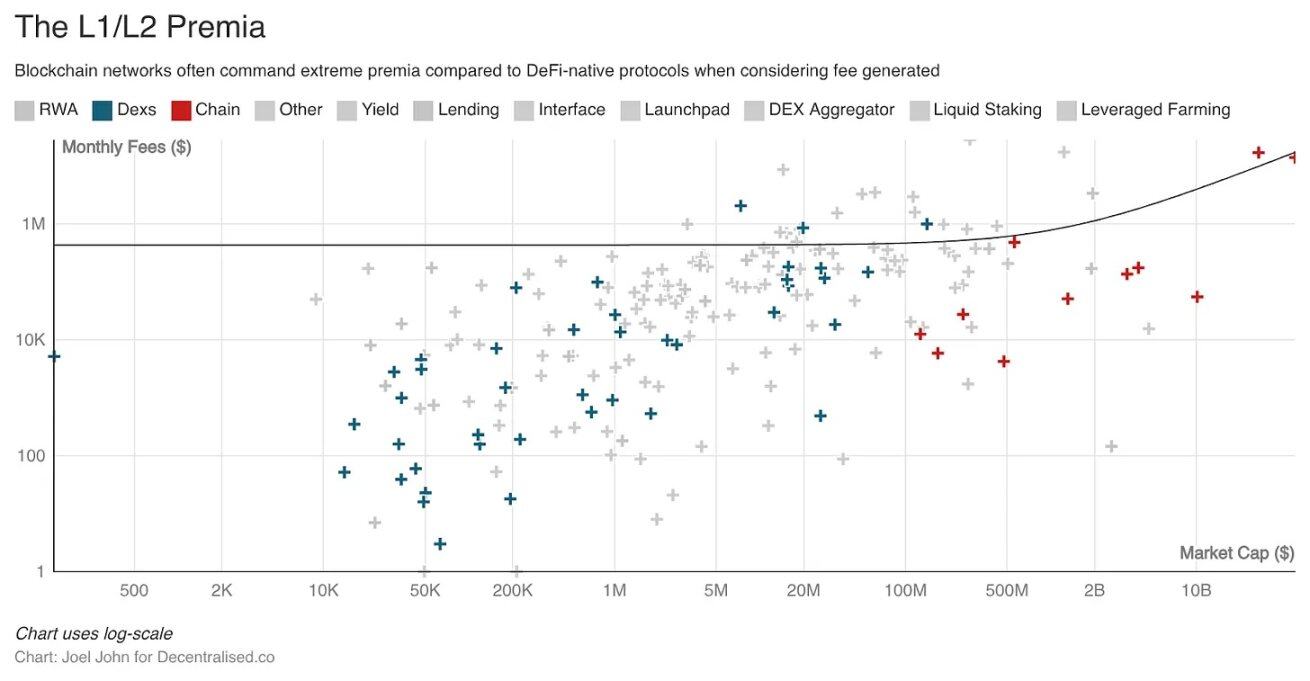

Historically, Layer 1 and Layer 2 chains commanded extremely high valuation premiums compared to standalone infrastructure. This premium, if used well, could have created new economies and funded developers to build truly useful applications. But open source + tokenization was too easy, leading to fifty homogeneous projects across thirty chains, with poor interoperability.

The fate of DeFi foundational components is even worse.

With too many choices for investors and novelty gone, valuations were halved even as economic activity increased.

Kamino, Euler, Fluid, Meteora, PumpSwap emerged, all with Price-to-Fees ratios far lower than in 2022. Some DEXs’ ratios even fell to 1x.

That is, the market values them below the fees they can generate in the next year.

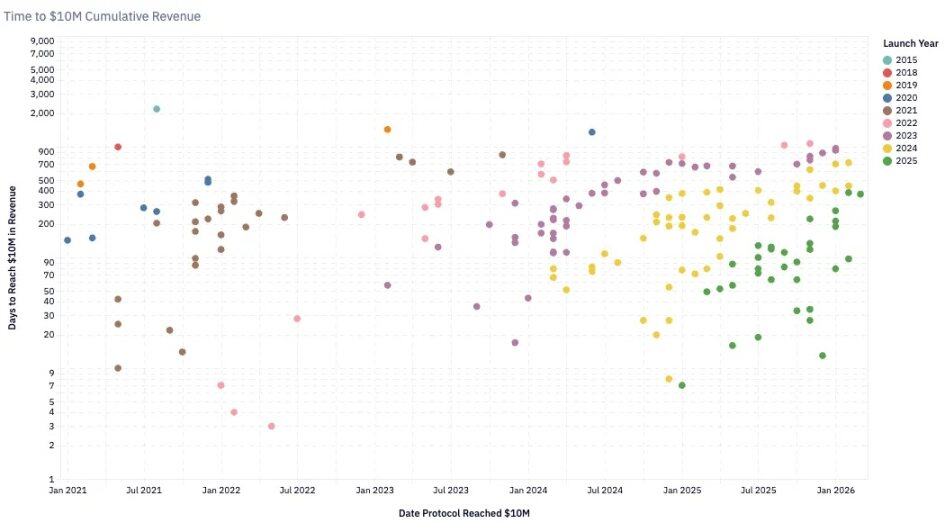

A bizarre paradox emerges: underlying protocols (DeFi components, public chains) see falling valuations, but applications built on top of them earn more money in less time.

The number of teams generating over $1 million in quarterly revenue has steadily risen, now exceeding 100.

In 2020, it took a protocol 24 months to reach $10 million in annual revenue, which was considered fast. By 2024, it took about 6 months. Pump.Fun, launched in early 2024, took only about two months to reach $10 million in revenue, setting a record.

This acceleration reflects both the maturity of underlying infrastructure (faster, cheaper) and the growing pool of capital on-chain chasing yield and entertainment.

For developers and entrepreneurs, the facts are clear:

- Nearly 900 protocols are making money today;

- Everyone is competing for median revenue, shares are smaller, but more teams overall are profitable;

- Median monthly revenue has dropped to $13,000.

The Three Moats of the Crypto Industry

Blockchain-native businesses have three types of moats:

- First-Mover Advantage

The early network effects of Tether and Circle are extremely difficult to replicate. They’ve weathered multiple cycles, forming a duopoly. Their businesses are non-tokenized and highly financialized. Tether is a centralized entity, with revenue primarily from US Treasuries.

- Liquidity Moat

Aave has maintained deep liquidity across cycles in an industry where capital is inherently yield-seeking. Hyperliquid is replicating this, but still needs time to prove itself. These protocols return funds to liquidity providers and optimize token governance.

- Distribution Moat

Seasonal applications like meme coin trading platforms rely on capital turnover and user demand. Web3 games and NFTs also fall into this category. With AI boosting productivity, small, focused teams can launch consumer-facing products faster. The core competency becomes: the ability to acquire and retain users when the market is hot.

Products built on distribution barriers can be immensely valuable but are outliers, not the norm. The value of traditional startups lies in replicable experience, like Y Combinator. But crypto iterates too fast for such experience to solidify.

This is also why it’s hard for entrepreneurs to replicate success in consumer products.

The cyclicality that once helped projects explode may not return. This isn’t to say entrepreneurs shouldn’t try. Data providers for prediction markets or smart economies might have excellent short-term cash flow.

But understand: this is a high-turnover, short-term game, not necessarily a lasting one. The trap is: raising blindly, or clinging to a token long after the hype has faded.

Questioning Governance: The Soul-Searching on Token Value

In 1999, many tech stocks had price-to-sales ratios of 10–20x. Akamai once reached 7434x. By 2004, it fell to 8x. A large number of companies fell from 30–50x to below 10x.

The dot-com bubble burst, evaporating trillions in speculative value. But many companies survived because the businesses were real.

Amazon fell 94%, later becoming one of the world’s most valuable companies. Crypto is undergoing the same valuation compression, just faster.

In 2020, DeFi was still experimental, with total annual revenue of only $21 million, and the overall market price-to-sales (P/S) ratio was a staggering 40,400x.

The market was full of fantasies about “what the future could be.”

In 2021, DeFi Summer turned revenue into real numbers, and P/S plummeted to 338x. Today, with annualized revenue of $18 billion, P/S is about 170x. In five years, compression from 40,400x to 170x.

But here’s a key question:

Visa’s P/S is about 18x, shareholders have dividends, buybacks, legally guaranteed profit rights and governance rights. Aave’s P/S is about 4x, but token holders only have governance rights, and only recently gained direct economic profit rights. Hyperliquid uses a rescue fund for buybacks, bringing HYPE holders closest to traditional equity holders. Aave also passed a $50 million annual buyback plan in 2025.

Artikel ini bersumber dari internet: When is the crypto industry most profitable, yet also most fearful?

The project with the largest single financing amount this period was Bitcoin mining company Canaan Technology, which announced the completion of a $39.75 million financing round. The second largest was cryptocurrency trading platform STS Digital, which announced the completion of a $30 million financing round. Furthermore, against the backdrop of the continued popularity of prediction markets, an increasing number of projects focused on the prediction market niche are emerging in the investment and financing field. The specific financing events are as follows (Note: 1. Sorted by the announced amount; 2. * indicates “traditional” companies with partial business involving blockchain): Canaan Technology Completes $39.75 Million Acquisition of Cipher Mining Project Equity Financing On February 24, Canaan Technology announced the completion of a $39.75 million financing round. By issuing 806,439,900 Class A…