Web3 Lawyer’s In-depth Policy Analysis|Hong Kong’s New Regulations for Virtual Asset Trading Platforms (Part 2): New Circular Issued, Are the Boundaries of Virtual Asset Business Redefined?

परिचय

At this point, some readers might wonder, can’t these services be offered in Hong Kong now? It feels like the train has already left the station, but looking back, why haven’t the tickets even started being sold?

As of now, only the 11 specialized platforms holding Virtual Asset Trading Platform (VATP) licenses can operate as virtual asset trading platforms in Hong Kong. Individual services like trading, investment advisory, and asset management for virtual assets have been made compliant by upgrading traditional licenses (Types 1, 4, 9), which is akin to building a temporary structure on top of the existing traditional licensing rules. The significance of the new regulations lies in pulling these important individual services out separately to establish dedicated licenses, each with its own clear responsibilities. Crypto Salad believes the signal released is quite clear: the regulation of virtual assets requires building a dedicated road, and it should be built separately.

However, the formal issuance of separate licenses is estimated to be around 2026. Looking back at this year, for licensed virtual asset trading platforms, the SFC issued two key circulars on November 3, 2025. Crypto Salad has previously analyzed one of them; for details, see “Web3 Lawyer’s In-depth Policy Analysis | New Regulations for Hong Kong Virtual Asset Trading Platforms (Part 1): Circular on Sharing Liquidity Among Virtual Asset Trading Platforms.” Today, let’s discuss the second part in detail: “Circular on Expanding the Products and Services of Virtual Asset Trading Platforms.”

1. What Does the Circular Say?

Those on the front lines of the industry can feel that real-world virtual asset business has clearly exceeded the original design scope of the VATP regulatory framework. The initial licensing system was designed purely around “centralized virtual asset trading platforms,” with a core focus on trade matching, client asset segregation, and maintaining basic market order. However, with the continuous emergence of stablecoins, tokenized securities, RWA, and various investment products linked to digital assets, the roles platforms play in practice have long ceased to be confined to pure trading venues.

Against this backdrop, the real contradiction facing regulators is no longer “whether these businesses should exist,” because if they continue to be left outside a clear regulatory framework, the market will evolve on its own in a gray area. Rather than letting practitioners find ways to circumvent the rules, it’s better to clearly define what can be done while simultaneously assigning corresponding responsibilities. We believe this is precisely the starting point of this circular.

In terms of specific content, the circular introduces several changes at the platform level that appear to be “deregulation” but are actually a reallocation of various responsibilities.

First, there is an adjustment to the token inclusion rules. Previously, for a virtual asset to be listed on a VATP platform, it typically needed to meet a requirement of at least 12 months of trading history. This standard essentially used time to filter risk. However, in practice, this approach is not always reasonable: a project’s longer existence does not necessarily mean sufficient information disclosure or controllable risk; conversely, a newly launched project is not necessarily lacking in adequate disclosure and prudent assessment.

It is important to note that this circular does not completely abolish the 12-month history requirement. Instead, it clearly provides exemptions under two specific circumstances:

First, for virtual assets offered only to professional investors. Second, for specified stablecoins issued by licensed issuers under the Hong Kong Monetary Authority (HKMA). In other words, the SFC has not denied the value of a trading history record. Instead, it acknowledges that risk assessment methods should not be one-size-fits-all for different investor groups and different asset types. Rather than using a formalistic time threshold to “block risk” for platforms, it is better to require platforms to take on more substantive judgment responsibilities themselves.

Accordingly, the circular also simultaneously strengthens disclosure requirements. For virtual assets lacking a 12-month history but offered only to professional investors, licensed platforms must clearly indicate this situation on their websites or applications and provide sufficient risk warnings.

The second important change is that the SFC has, for the first time at the license condition level, explicitly stated that VATP platforms can, subject to compliance with the existing regulatory framework, distribute tokenized securities and investment products related to digital assets.

Currently, VATPs in reality already function similarly to “product gateways.” Once they enter this new distribution role, platforms will no longer face only counterparty risk but also typical financial product distribution responsibilities, including product understanding, suitability assessments, and information disclosure obligations. This is not a regulatory concession but a change in responsibility resulting from the change in role.

The third adjustment focuses on custody rules. The circular allows licensed platforms, through their associated entities, to provide custody services for virtual assets or tokenized securities that are not traded on the platform.

What changes will this bring? In current practice, assets from many projects do not necessarily need to be traded on a platform, but clients still wish to have regulated institutions hold or manage these assets. Therefore, designing for such demand has not been smooth, often requiring complex multi-layered arrangements to barely achieve it. After the circular takes effect, it essentially provides a clearer compliance path for these existing business needs.

If the main body of the circular outlines the overall policy direction, then the three appendices reflect more of the SFC’s considerations on “how to implement” at the operational level.

Appendix I, which revises the token inclusion rules, appears to lower the listing threshold for some products but does not substantially weaken the platform’s prudential obligations. The threshold hasn’t disappeared; VATPs now need to support their judgments with more solid due diligence and disclosure.

The above image is a screenshot from the Hong Kong SFC official website.

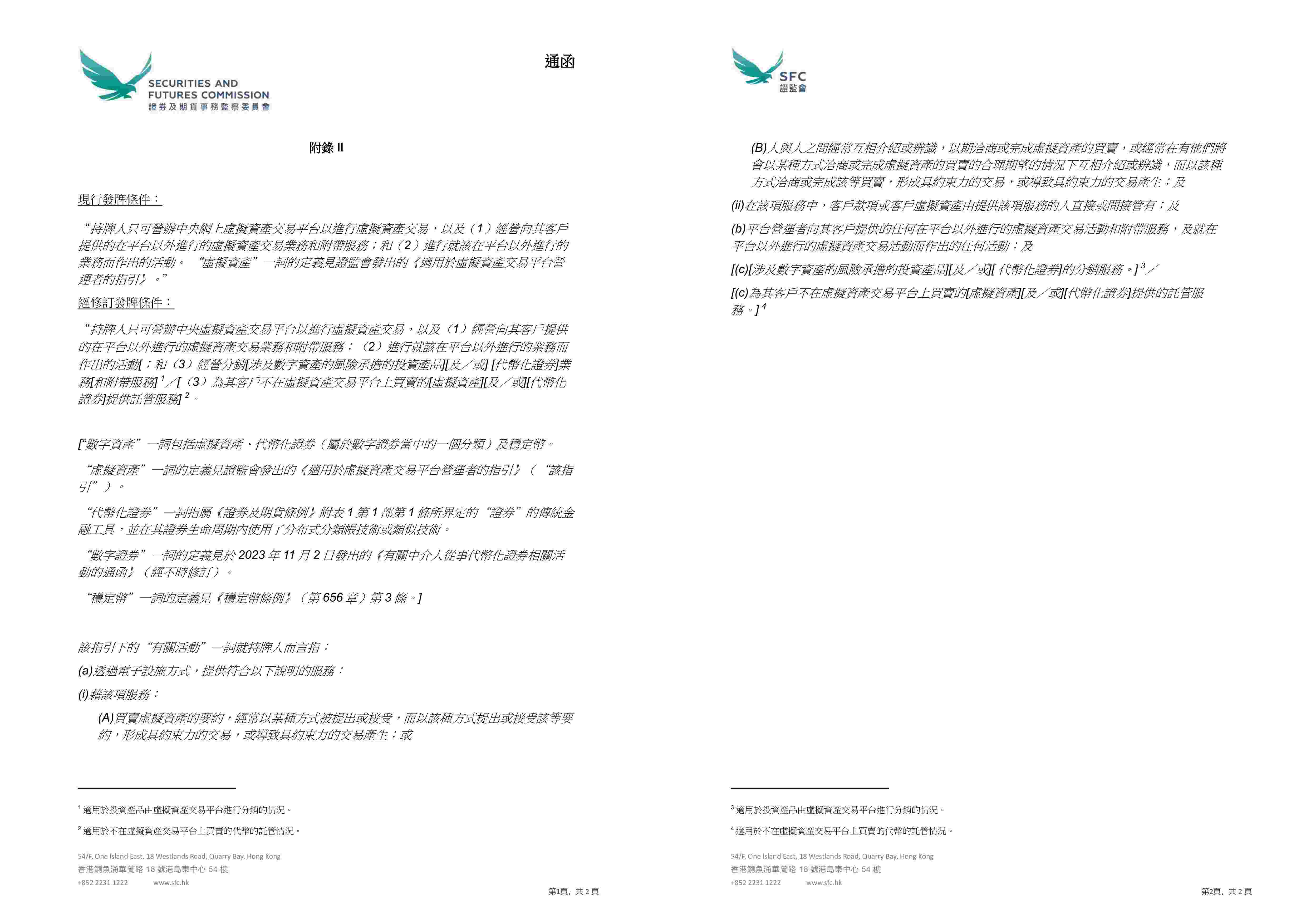

Appendices II and III further clarify the boundaries of a platform’s business scope and the arrangements for holding client assets during the distribution process. By redefining “relevant activities,” the SFC formally includes the distribution of digital asset-related investment products, tokenized securities, and custody services for assets not traded on the platform within the scope of VATP operations. Simultaneously, in distribution business, platforms are allowed to open and maintain trust accounts or client accounts in their own name with relevant custodians to hold these assets on behalf of clients. These adjustments do not lower the requirements for client asset protection but rather make the business structure legally and regulatorily “workable.”

The above image is a screenshot from the Hong Kong SFC official website.

2. After the Circular, What Changes Should Practitioners Note?

With the issuance of the new circular, for VATPs, activities that were previously bundled together—such as trading, custody, research, product introduction, and even some distribution activities—under the umbrella of “platform services,” as long as they were covered by the VATP license, must now be more clearly distinguished. They must identify which behaviors belong to the core functions of an exchange and which are closer to independent custody, distribution, or investment advisory activities. Compliance must then be achieved through corresponding entity arrangements and business boundary delineations.

For other participants, such as OTC desks and custody service providers, the room for operation that relied on ambiguous roles or mixed functions is rapidly narrowing. They must now more clearly answer a question: What specific type of virtual asset service are they engaged in? And under which regulatory framework should they assume corresponding responsibilities?

3. निष्कर्ष

Overall, this circular does not reflect a sudden shift in regulatory attitude but rather a more pragmatic choice: VATP platforms are gradually evolving from single trading venues into compliance nodes connecting trading, products, and asset management. Correspondingly, regulatory focus is shifting from formalistic conditions to whether platforms truly shoulder their due responsibilities.

This circular does not mean business is “deregulated” overnight. However, the change in regulatory attitude is clear: compliance is no longer just about “not crossing the line” but about being responsible for one’s own judgments. For project teams and investors, it also means regulatory expectations are gradually becoming clearer, rather than continuing to rely on ambiguous spaces for survival.

Moving forward, how far the market can go no longer depends on whether regulators provide space, but on whether participants are truly prepared to operate under a clearer and more serious set of rules.

Special Disclaimer: This article is an original work by the Crypto Salad team and represents only the personal views of the author. It does not constitute legal consultation or advice on specific matters. For authorization to reprint this article, please contact via private message: shajunlvshi.

यह लेख इंटरनेट से लिया गया है: Web3 Lawyer’s In-depth Policy Analysis|Hong Kong’s New Regulations for Virtual Asset Trading Platforms (Part 2): New Circular Issued, Are the Boundaries of Virtual Asset Business Redefined?

Related: Verse8’s own account: How to support creative expression in the AI era

Verse8 is an AI-native creation layer that transforms your ideas into interactive games and stories. Every creation can be owned, recreated, and its value continuously accumulated. Just as OpenAI started with chat, Runway rose to prominence with video, and Stability made its breakthrough with images, Verse8 opens up in the most representative form: interactive content. Games are just the first vertical field to shine in this new medium. We believe that creation should be accessible to everyone, not just developers. Why we built Verse8 Interactive content creation has always been one of the most difficult fields to enter: long production cycles, high upfront costs, and a complex process requiring collaboration among coders, designers, and artists. Current systems are not creator-friendly. However, creativity should not be stifled. When we realized that…